What is a chargeback?

Chargebacks have an important role to play in the payments ecosystem. They give consumers recourse against fraud and errors, which preserves public confidence in credit and debit card payments. This is especially significant in e-commerce, where the risk of third-party and merchant fraud is perceived to be much higher.

The downside of chargebacks is that they can be a huge, costly headache for the merchants who have to deal with them. Many consumers ask for chargebacks over problems that chargebacks were never intended to address, or dispute transactions without even attempting to contact the merchant first.

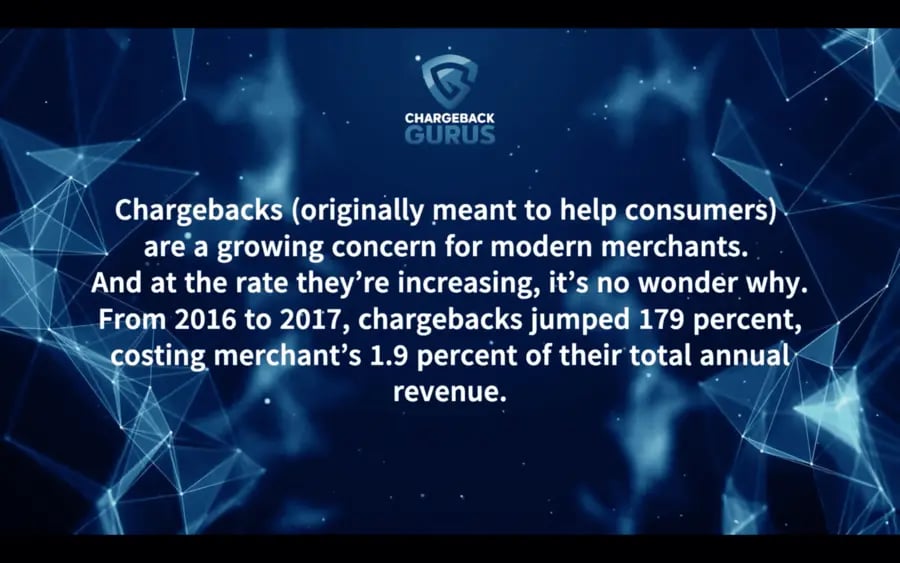

Global chargeback rates keep increasing year-to-year, and recent gains in e-commerce have led to a commensurate increase in fraud and chargeback activity. With chargebacks on the rise, more businesses are taking action to defend themselves. What are chargebacks, and what do merchants need to know in order to prevent and fight them as effectively as possible?

If you have any questions about how to protect your business from chargebacks, please feel free to reach out to us directly.

- What is a Chargeback?

- How Do Chargebacks Work?

- What is the Chargeback Process?

- What Do Chargebacks Mean for Merchants?

- How Many Chargebacks Occur Annually?

- How Do Cardholders File a Chargeback?

- Why Do Customers File Chargebacks?

- When Can a Cardholder Legitimately Dispute a Charge?

- What are Chargeback Reason Codes?

- American Express Chargeback Reason Codes

- Visa Chargeback Reason Codes

- Mastercard Chargeback Reason Codes

- Discover Chargeback Reason Codes

- What are the Three Types of Chargebacks?

- What is the EMV Liability Shift?

- Who is Liable for Chargebacks?

- Should Merchants Fight Chargebacks?

- How Do You Write a Chargeback Rebuttal Letter?

- Can You Prevent all Chargebacks?

- How Much are Chargeback Fees?

- Know the Facts about Chargebacks

- What’s the Difference between a Chargeback and a Refund?

- How Long Do You Have to Fight a Chargeback?

- What is a Chargeback Threshold?

What is a Chargeback?

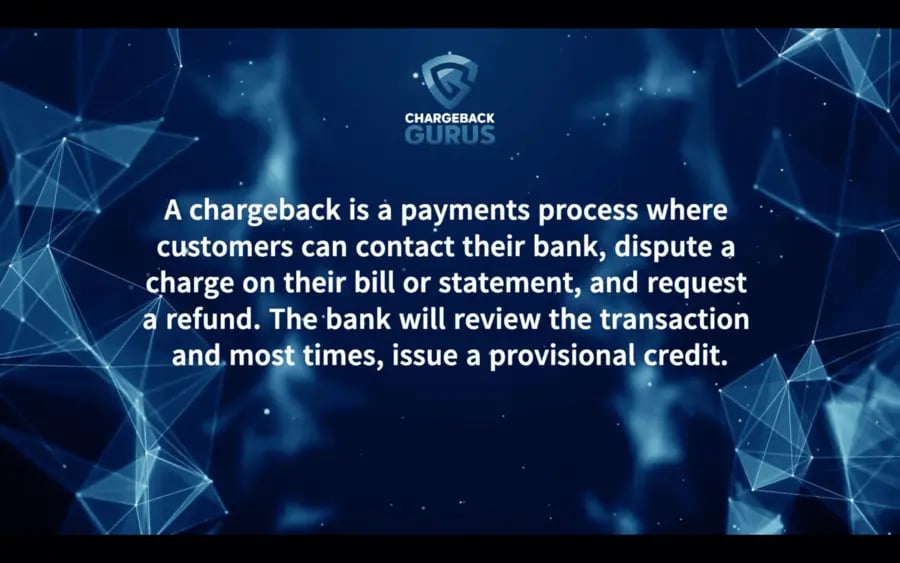

A chargeback is the potential outcome of a disputed credit or debit card transaction. If the cardholder’s bank accepts the dispute, they will reverse the transaction, taking the funds back from the merchant and returning them to the cardholder.

When a cardholder disputes a charge, their issuing bank will review the transaction and decide if the dispute is valid. If they believe that it is, they will provide the cardholder with a provisional credit and work with the card network and the acquiring bank to finalize a chargeback.

Chargebacks for credit cards were first implemented in the 1974 Fair Credit Billing Act (§ 161. Correction of billing errors), an amendment to the Truth in Lending Act.

Chargebacks for credit cards were first implemented in the 1974 Fair Credit Billing Act (§ 161. Correction of billing errors), an amendment to the Truth in Lending Act.

Debit card chargebacks were implemented later by the Electronic Fund Transfer Act in 1978. These acts were intended to outline protective measures for consumers.

Chargebacks were created in response to widespread abuse by fraudsters who would use stolen credit card information to make purchases. Before the Fair Credit Billing Act, there wasn’t much cardholders could do to get their money back from merchants who had received these fraudulent payments.

The chargeback process allows consumers to get their refunds from their banks, and to let banks (rather than cardholders and merchants) make decisions on how to handle the situation. While the process was not yet called a chargeback, it would become the foundation for the dispute system we know today.

How Do Chargebacks Work?

Chargebacks are initiated by cardholders, evaluated by banks, and paid for by merchants. A single chargeback, from initiation to resolution, can last months or even years.

While banks will sometimes file chargebacks for things like authorization or processing errors, most chargebacks occur when a cardholder contacts their bank to dispute a charge on their account. Usually, they do this because they don’t recognize the charge and believe it to be fraudulent.

In some cases, a cardholder might dispute a charge because they feel they didn’t get what they paid for and the merchant has refused to resolve the issue.

Once a chargeback has been initiated, it will go back and forth between the issuing bank and the merchant until either one of them agrees to accept liability or until the card network must be called in to resolve the dispute.

What is the Chargeback Process?

- When a cardholder disputes a transaction with their issuing bank, the bank decides whether or not the customer has grounds to file a chargeback.

- If a chargeback is granted, the bank will notify the acquiring bank—AKA the merchant’s bank—and debit the funds from the merchant’s account.

- The merchant can either accept the chargeback or fight it by resubmitting the charge along with a rebuttal letter and the necessary evidence to disprove the claim. This process is called representment.

- The issuing bank will review the new evidence and make a decision. If they find in favor of the merchant, the funds will be returned.

- At this point, any party unhappy with the decision can contest the issue further by initiating pre-arbitration. This most often occurs when the issuing bank decides in the merchant’s favor, but then receives new evidence that puts that decision in question.

- If neither party accepts liability during pre-arbitration, the chargeback moves to arbitration. Here, the card network will examine the evidence and make a final decision. This decision can’t be appealed further, and the losing party will be required to pay hundreds of dollars in fees.

Time limits for merchants to respond to a dispute vary based on the credit card network and the reason code. Note that the timer begins when the chargeback is initiated, not when the merchant is notified, so the merchant’s deadline may not be the exact time frame outlined by the card network’s policies.

What Do Chargebacks Mean for Merchants?

If a merchant’s chargeback ratio exceeds certain thresholds established by the card networks and other financial institutions they do business with, they may face fines, additional chargeback fees, and even termination of their merchant account. The most common threshold is 1%, but Visa recently lowered theirs to 0.9%.

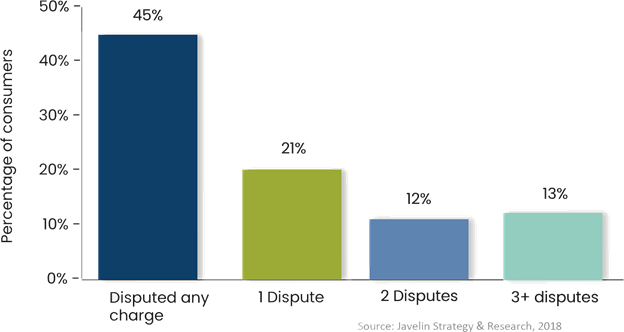

How Many Chargebacks Occur Annually?

We do have some data from a 2018 survey by Javelin Research showing that nearly half of all customers have disputed a charge, and a majority of those have disputed more than one.

We also know that chargebacks continue to grow year after year. A 2018 study by Aite Group predicted that the total value of chargebacks would climb to $35 billion by 2021, and given the increase in disputes that accompanied the COVID-19 pandemic, it wouldn’t be surprising to find we’ve already far exceeded that number.

How Do Cardholders File a Chargeback?

The bank will typically give the cardholder a provisional credit for the amount of the charge while they investigate the validity of the claim. The cardholder should be prepared to describe the problems they had with the merchant and the steps they took to resolve the matter.

Why Do Customers File Chargebacks?

In order to identify the reason a customer disputed a charge, it can be helpful to examine the reason code on the chargeback.

Every chargeback has a reason code associated with it. The major card networks (Visa, Mastercard, Discover, and American Express) established these codes to clearly identify the reason a chargeback was requested.

What are Chargeback Reason Codes?

While the reason code will tell you how the cardholder justified the dispute to their bank, it’s important to keep in mind that this isn’t always the real reason for the chargeback.

Some customers may incorrectly think that a charge on their account was unauthorized because they don’t recognize the name of the business listed in the transaction description. Others may have forgotten about a recurring charge they signed up for.

There are also some customers who want to file a chargeback because of a negative experience they had with the merchant, but know that the reason they have isn’t a legitimate basis for a dispute. In order to get the chargeback, they lie to the bank about their reason for requesting one. In some cases, a customer may have made a purchase with the intention of fraudulently disputing the charge later in an effort to get their money back.

When Can a Cardholder Legitimately Dispute a Charge?

If a cardholder is a victim of true fraud (unauthorized use of stolen credit card credentials), then a chargeback is most legitimate and ethical way for the issuing bank and the merchant to resolve the issue.

Customers can also file chargebacks when they didn’t receive the product or service they paid for, whether because of a lost or damaged shipment or an incorrect item being sent. Being double-charged or overcharged the agreed purchase amount is another legitimate reason for a dispute.

Customers can also file chargebacks when they didn’t receive the product or service they paid for, whether because of a lost or damaged shipment or an incorrect item being sent. Being double-charged or overcharged the agreed purchase amount is another legitimate reason for a dispute.

However, problems like these are usually resolved more quickly and easily when the customer contacts the merchant, and a chargeback should only be used when the merchant is uncooperative.

Then there are the customers commit first-party misuse, better known as "friendly fraud," by filing a chargeback without a legitimate reason.

Customers can’t dispute a charge simply because they are dissatisfied with the product or service they received. These issues must always be resolved with the merchant directly.

American Express Chargeback Reason Codes

Learn how to fight each of these American Express Chargeback Codes >>>

| Chargeback Code | Description |

| Authorization | |

| A01 | Charge Amount Exceeds Authorization Amount |

| A02 | No Valid Authorization |

| A08 | Authorization Approval Expired |

| Fraud | |

| F10 | Missing Imprint |

| F14 | Missing Signature |

| F24 | No Card Member Authorization |

| F29 | Card Not Present |

| F30 | EMV Counterfeit |

| F31 | EMV Lost/Stolen/Non-Received |

| Card Member Dispute | |

| C02 | Credit Not Processed |

| C04 | Goods/Services Returned or Refused |

| C05 | Goods/Services Cancelled |

| C08 | Goods/Services Not Received |

| C14 | Paid by Other Means |

| C18 | “No Show” or CARDeposit Cancelled |

| C28 | Cancelled Recurring Billing |

| C31 | Goods/Services Not as Described |

| C32 | Goods/Services Damaged or Defective |

| Processing Error | |

| P01 | Unassigned Card Number |

| P03 | Credit Processed as Charge |

| P04 | Charge Processed as Credit |

| P05 | Incorrect Charge Amount |

| P07 | Late Submission |

| P08 | Duplicate Charge |

| P22 | Non-Matching Card Number |

| P23 | Currency Discrepancy |

| Inquiry/Miscellaneous | |

| R03 | Insufficient Reply |

| R13 | No Reply |

| M01 | Chargeback Authorization |

| M10 | Vehicle Rental - Capital Damages |

| M49 | Vehicle Rental - Theft or Loss of Use |

| FR2 | Fraud Full Recourse Program |

| FR4 | Immediate Chargeback Program |

| FR6 | Partial Immediate Chargeback Program |

Visa Chargeback Reason Codes

Learn how to fight each of these Visa Chargeback Codes >>>

| Chargeback Code | Description |

| Fraud | |

| 10.1 | EMV Liability Shift Counterfeit Fraud |

| 10.2 | EMV Liability Shift Non-Counterfeit Fraud |

| 10.3 | Other Fraud — Card Present Environment |

| 10.4 | Other Fraud — Card Absent Environment |

| 10.5 | Visa Fraud Monitoring Program |

| Authorization | |

| 11.1 | Card Recovery Bulletin |

| 11.2 | Declined Authorization |

| 11.3 | No Authorization |

| Processing Errors | |

| 12.1 | Late Presentment |

| 12.2 | Incorrect Transaction Code |

| 12.3 | Incorrect Currency |

| 12.4 | Incorrect Account Number |

| 12.5 | Incorrect Amount |

| 12.6.1 | Duplicate Processing |

| 12.6.2 | Paid by Other Means |

| 12.7 | Invalid Data |

| Consumer Disputes | |

| 13.1 | Merchandise/Services Not Received |

| 13.2 | Cancelled Recurring |

| 13.3 | Not as Described or Defective Merchandise/Services |

| 13.4 | Counterfeit Merchandise |

| 13.5 | Misrepresentation |

| 13.6 | Credit Not Processed |

| 13.7 | Cancelled Merchandise/Services |

| 13.8 | Original Credit Transaction Not Accepted |

| 13.9 | Non-Receipt of Cash or Load Transaction Value |

Mastercard Chargeback Reason Codes

Learn how to fight each of these Mastercard Chargeback Codes >>>

| Code | Description |

| Authorization | |

| 4808 | Required Authorization Not Obtained |

| 4808 | Expired Chargeback Protection Period |

| 4808 | Multiple Authorization Requests |

| 4808 | Cardholder-Activated Terminal (CAT) 3 Device |

| Point of Interaction Error | |

| 4834 | Transaction Amount Differs |

| 4834 | Late Presentment |

| 4834 | Point-of-Interaction Currency Conversion |

| 4834 | Cardholder Debited More than Once for the Same Goods or Services |

| 4834 | ATM Disputes |

| 4834 | Loss, Theft, or Damages |

| Fraud | |

| 4837 | No Cardholder Authorization |

| 4849 | Questionable Merchant Activity |

| 4870 | EMV Chip Liability Shift |

| 4871 | EMV Chip/PIN Liability Shift |

| Cardholder Disputes | |

| 4853 | Cardholder Dispute of a Recurring Transaction |

| 4853 | Issuer Dispute of a Recurring Transaction |

| 4853 | Goods or Services Not Provided |

| 4853 | No-Show Hotel Charge |

| 4853 | Addendum Dispute |

| 4853 | Credit Not Processed |

| 4853 | Goods/Services not as Described or Defective |

| 4853 | Digital Goods $25 or less |

| 4853 | Counterfeit Goods |

| 4853 | Transaction Did Not Complete |

| 4853 | Credit Posted as a Purchase |

| 4853 | Timeshares |

| 4854 | Cardholder Dispute Not Classified Elsewhere |

| Other | |

| 4850 | Installment Billing Dispute (Participating Countries Only) |

| 4999 | Domestic Chargeback Dispute (Europe Region Only) |

Discover Chargeback Reason Codes

Learn how to fight each of these Discover Chargeback Codes >>>

| Chargeback Code | Description |

| Fraud | |

| UA01 | Fraud – Card Present Transaction |

| UA02 | Fraud – Card Not Present Transaction |

| UA05 | Fraud – Chip Counterfeit Transaction |

| UA06 | Fraud – Chip and PIN Transaction |

| UA10 | Request Transaction Receipt (swiped card transactions) |

| UA11 | Cardholder Claims Fraud (swiped transaction, no signature) |

| Authorization | |

| NA | No Authorization |

| DA | Declined Authorization |

| AT | Authorization Non-Compliance |

| EX | Expired Card |

| Processing Errors | |

| IN | Invalid Card Number |

| LP | Late Presentation |

| Services | |

| 5 | Good Faith Investigation |

| AA | Does Not Recognize |

| AP | Recurring Payments |

| AW | Altered Amount |

| CD | Credit/Debit Posted Incorrectly |

| DP | Duplicate Processing |

| IC | Illegible Sales Data |

| NF | Non-Receipt of Cash from ATM |

| PM | Paid by Other Means |

| RG | Non-Receipt of Goods, Services, or Cash |

| RM | Cardholder Disputes Quality of Goods or Services |

| RN2 | Credit Not Processed |

| Other | |

| DC | Dispute Compliance |

| NC | Not Classified |

What are the Three Types of Chargebacks?

True Fraud

True fraud chargebacks are what chargebacks were invented for: unauthorized charges against a credit card by a scammer or identity thief. Merchants are strongly advised not to waste time or resources attempting to dispute these chargebacks.

True fraud chargebacks are best prevented through fraud prevention tools. AVS and CVV matching are the bare minimum, but many merchants also use multi-factor authenticators like 3-D Secure or third-party tools that use artificial intelligence and machine learning to weed out fraudulent transactions.

Friendly Fraud

Friendly fraud chargebacks are when customers report valid charges as fraudulent to get the charge reversed. They might do this deliberately, with malicious or criminal intent, or they might do it out of impatience or confusion. Friendly fraud chargebacks often masquerade as true fraud chargebacks, with the customer falsely claiming they never authorized the charge.

These chargebacks are difficult to prevent, but can be fought through representment to recover lost revenue. Customers who file friendly fraud chargebacks can also be blacklisted.

Merchant Error

Merchant error chargebacks occur when the cause of the chargeback is an error made by the merchant, such as shipping the wrong item. Disputes like this can sometimes be fought effectively, but the flaws in merchant operations these chargebacks reveal must be remedied to prevent similar future chargebacks.

Merchant error chargebacks can be prevented by improving business operations, by providing helpful customer service 24/7, and by having a generous refund policy.

What is the EMV Liability Shift?

The basic idea is that if an EMV card is used fraudulently and the merchant had not upgraded their processing equipment to EMV-compliant standards, the blame for that fraudulent transaction lies with the merchant.

The EMV Liability Shift caused most merchants to upgrade to EMV payment technology, which is much less vulnerable to fraud than traditional magnetic strips. However, it may also have resulted in an increase in fraudulent chargebacks. Savvy fraudsters have learned that if they convince a merchant to swipe a card with an EMV chip and later dispute that charge, the merchant will lose the dispute.

Who is Liable for Chargebacks?

For card-present merchants, if the purchase is made using an EMV chip and the transaction turns out to be fraudulent, the issuing bank is held liable instead of the merchant. The merchant is still responsible for chargebacks arising due to merchant errors.

Should Merchants Fight Chargebacks?

When a merchant knows that a chargeback is illegitimate, they should fight back through the chargeback representment process. As long as the merchant has the evidence required to disprove the false claims, they should be able to recover their losses.

Merchants who receive a chargeback that they believe is unfounded have the right to contest the case. To do so, they’ll first need to submit a rebuttal letter to argue their case, along with a number of supporting documents and pieces of evidence. Exactly what evidence they’ll need will depend on the exact reason code associated with the chargeback.

When a merchant contests a cardholder chargeback, it then enters representment. During this process, the merchant provides information about the transaction and explains why they believe it was legitimate.

The merchant works with their sales  department and/or their chargeback management company to build a dispute package that outlines the evidence and attempts to convince the issuing bank according to that bank’s guidelines.

department and/or their chargeback management company to build a dispute package that outlines the evidence and attempts to convince the issuing bank according to that bank’s guidelines.

Following this, the acquiring bank sends the information back through the credit card network to the issuing bank, who makes their decision and informs the involved parties.

If you plan to dispute a chargeback, it’s important to act quickly. Issuers often lag behind when notifying acquirers and merchants of chargebacks, so you may have a very small window in which to respond. Having a chargeback representment team at your disposal can help you act swiftly and efficiently, no matter what the deadline may be.

How Do You Write a Chargeback Rebuttal Letter?

A prompt rebuttal letter can help you better address fraudulent chargebacks and win disputes. When done right, a rebuttal letter provides a simple overview of why the customer’s claims are false and what evidence you have to prove it. When disputing friendly fraud chargebacks, a good rebuttal letter combined with sufficient evidence will typically convince the issuing bank to rule in your favor and return your revenue.

Can You Prevent All Chargebacks?

Studying and fighting disputes will help you learn why they’re happening to you, and addressing those root causes is by far the best thing you can do to prevent future chargebacks.

How Much are Chargeback Fees?

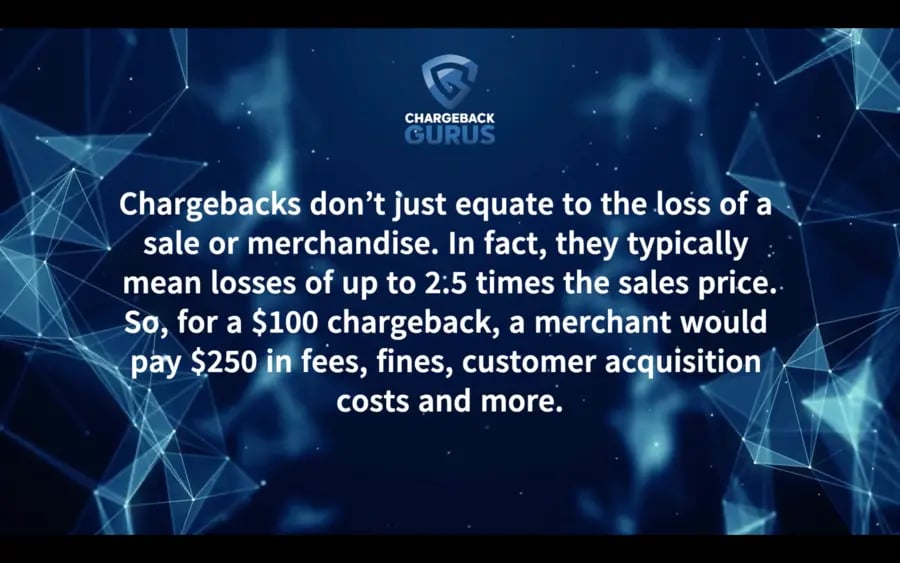

| Expense | Physical Goods |

Digital Goods & Services

|

| Transaction Cost | $250 | $250 |

| Processing Fee | $10 | $10 |

| Chargeback Fee | $25 | $25 |

| Product/Service Cost | $75 | $50 |

| Marketing Cost | $100 | $100 |

| Fraud Management Cost | $5 | $5 |

| Fulfillment Cost | $5 | $3 |

| Customer Service Cost | $2 | $2 |

| Operations Cost | $50 | $35 |

| Total Revenue Loss | $522 | $480 |

| True Cost | 2.1x | 1.92x |

Chargebacks can threaten your cash flow and put your merchant accounts at risk, too. They can increase your merchant account costs or cause your accounts to be shut down, preventing you from accepting payments altogether.

Know the Facts about Chargebacks

When you understand what chargebacks are, you can fight them more effectively, learn from them, and take steps to prevent them. Even when choosing a chargeback management firm to deal with them for you, having a solid grounding in the facts about chargebacks will help you know whether that firm is providing you with a good return on your investment.

Regardless of your level of experience with chargebacks, Chargeback Gurus can guide you to the best possible outcomes for your company. Download your copy of the Chargebacks 101 Guide to better help you understand the root causes of disputes and how the overall chargeback process works. Armed with that knowledge, you'll be able to prevent avoidable disputes and fight fraudulent chargebacks.

FAQ

What’s the difference between a chargeback and a refund?

How long do you have to fight a chargeback?

What is a chargeback threshold?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com