Merchant Account Fees and Your Bottom Line

After months of planning and research, your online store is open and ready for business. Your website is attractive on any device. The sale price of your shiny, new product is competitive, and now that you have set up your merchant account, your customers can make purchases by credit card. It was a long process to arrive at your opening day milestone, but your new business is launched! In a few months, based on your sales and expenses, you will be able to determine your ongoing profitability.

Several of your business expenses may be challenging to predict. For example, some merchant account processing fees are variable and others are transactional. Furthermore, even if you negotiated the terms before you signed the agreement, you may find some surprising charges on your monthly merchant account statement.

One of the complicated and unpredictable charges that processors collect is called a bill-back fee. A bill-back fee is an additional processing charge on a prior card transaction. According to your merchant agreement, out-of-the-ordinary transactions may trigger an additional processing charge. A few examples of transactions that can incur bill-back pricing are purchases made by a gift or rewards card, a keyed instead of a swiped card, or a business card purchase.

For billing ease, processors initially charge you a fixed rate for all card transactions processed during your billing period. Then, the following month, processors will bill you for additional fees incurred on eligible transactions that were processed the previous month. Being billed in two separate months for the same transaction can be confusing. This is because bill-back fees often appear on your monthly statement in the month after the original interchange fee was billed to you. So, to determine the total processing cost of an individual transaction, you may need to compare two monthly statements side by side.

For instance, MasterCard and VISA fees are not always equal and could be higher than your fixed, flat discount rate. Let’s say your processor charges a flat card transaction rate of 1.5%, and the cost of a MasterCard transaction is actually 1.75%. In the first month the transaction is processed, you would be billed the flat rate of 1.5%. Then, in the following month, your processor would bill you back the difference, or .25%.

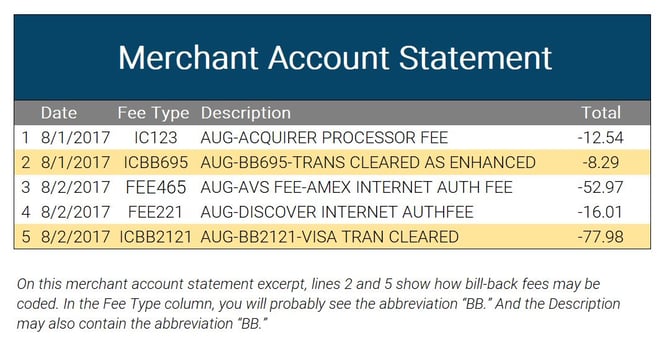

The good news for determining your bottom line is that bill-back charges are not hidden. You can identify them on your merchant account statement. Bill-back fees are usually listed in the “Interchange” section and are marked with the code “BB.”

Once you are able to spot bill-back charges, you can determine the actual total cost of accepting credit card payments and, therefore, manage your profit margin. Then, if you think you are paying too much in bill-back fees, you will have the opportunity to approach your processor and negotiate more favorable bill-back terms.