Difference Between Chargebacks & Retrieval Requests

Table of Contents

- Chargebacks

- How Chargebacks Work

- Retrieval Requests

- How Retrieval Requests Work

- Respond to retrieval Requests, Prevent Chargebacks

- Frequently Asked Questions

It’s easy to confuse chargebacks with retrieval requests, since news of both comes directly from a merchant’s bank.

But in terms of impact, the two occurrences are very different. While one can have a serious impact on your bottom line and financial health as a merchant, the other might simply be a request for further information. In some cases, it may even be an opportunity to prevent a chargeback from occurring altogether, thus saving your business time, energy, and most importantly, resources. Knowing the difference between the two terms—as well as what causes both of them to happen—can help you address your growing chargeback problems from the ground up.

Knowing the difference between the two terms—as well as what causes both of them to happen—can help you address your growing chargeback problems from the ground up.

Chargebacks

A chargeback is the result of a consumer disputing a charge with their bank or card issuer.

They may have seen a transaction on their account statement that they didn’t recognize, or they may be unhappy with their purchase or service. In some cases, chargebacks occur because the consumer is trying to get something for free. Other times the purchase was made with stolen credit card information, and the cardholder is looking to recover their losses.

Chargebacks result in the transaction being reversed by withdrawing funds from the merchant's account. Although those funds can be recovered by winning a dispute, the merchant will be responsible for paying a chargeback fee regardless of whether they win or lose.

How Chargebacks Work

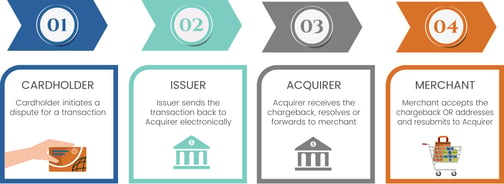

The chargeback process is a four-step one, involving the consumer, the card issuer, the merchant and the merchant’s bank. In the event the merchant has a chargeback representment firm on their side, the firm will take part in this process as well.

Here’s what the chargeback process looks like:

- The cardholder disputes a transaction with their bank or card issuer

- The issuer sends the transaction back to the merchant’s bank, also called the acquiring bank

- The acquiring bank receives the chargeback, then either resolves it or sends it on to the merchant for review

- The merchant receives notification of the chargeback. They can either accept the chargeback as-is or address it by offering evidence to the acquiring bank that proves the transaction is valid

Retrieval Requests

Merchants can also receive notification of retrieval requests from their bank, though the two happenings don’t have the same repercussions.

Often called “soft chargebacks,” retrieval requests simply indicate that a consumer wants more information about a transaction or purchase.

They might have spotted an unknown charge on their account but can’t remember what they bought. In this case, they would submit a retrieval request to get more information on that transaction before filing a full-on chargeback dispute. The important thing to note is that a retrieval request is an opportunity to issue a proactive refund ahead of a potential chargeback. But even if a merchant doesn’t issue a refund, responding to a retrieval request in some fashion is vital. Failing to respond to a retrieval request disqualifies a merchant from disputing a chargeback. In the event a chargeback is filed, they have no choice but to accept the financial losses associated with it

The important thing to note is that a retrieval request is an opportunity to issue a proactive refund ahead of a potential chargeback. But even if a merchant doesn’t issue a refund, responding to a retrieval request in some fashion is vital. Failing to respond to a retrieval request disqualifies a merchant from disputing a chargeback. In the event a chargeback is filed, they have no choice but to accept the financial losses associated with it

How Retrieval Requests Work

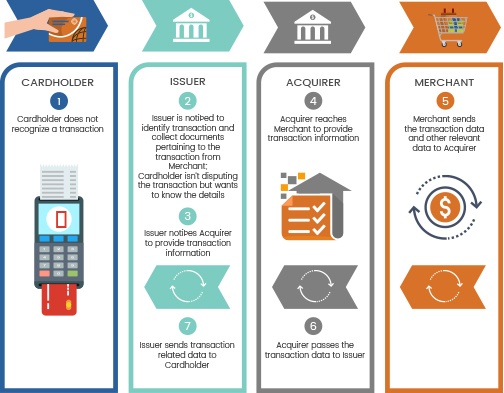

The retrieval request process starts just like a chargeback. The customer calls their issuing bank about an unknown transaction and asks for additional information on the charge.

The rest of the process looks like this:

- The issuing bank notifies the merchant’s bank that a retrieval request has been made

- The acquiring bank reaches out to the merchant to get more information on the transaction in question

- The merchant sends all transaction data back to their bank. This can include receipts, invoices, tracking numbers, shipment information and any other data they might have on the transaction

- The acquiring bank then passes that data onto the issuer, who sends it on to the cardholder

Merchants should be thorough when responding to retrieval requests, as these are often the first step toward a true chargeback dispute.

Offering thorough, comprehensive information on a transaction can help prevent consumers from filing those disputes and hurting a merchant’s bottom line.

If a merchant opts to offer a proactive refund on a retrieval request in an attempt to prevent future chargebacks, they should notify their issuing bank and include the ARN, as well as both the original transaction receipt and the refund receipt, in their response.

Respond to Retrieval Requests, Prevent Chargebacks

Merchants who fail to take adequate measures to prevent chargebacks can face significant losses. For one thing, every chargeback, win or lose, comes with a chargeback fee. Even more importantly, however, many of the parties involved in the payment process set thresholds for chargeback ratios which, if exceeded, may result in severe penalties.

The reserve requirement for a merchant account being increased is a common result of a high chargeback ratio. If the rate of chargebacks climbs high enough, the merchant account may even be terminated. Merchants may also have more difficulty processing payments, or be dropped by processors entirely.

Understanding retrieval requests and how to respond to them can be a key way to prevent chargebacks, but it's just one small part of a comprehensive chargeback prevention program. In order to prevent as many chargebacks as possible and protect your business, it's also important to understand the reasons chargebacks are occurring, maintain monitoring of chargebacks and transactions, and keep thorough records to give the best possible chance of winning friendly fraud disputes.

If that feels like a bit of an overwhelming task to handle on your own, you may wish to consider professional chargeback management services. A team of experts can analyze your chargeback data to find the best methods for fraud detection and chargeback prevention, and can use their expertise to determine which chargeback disputes to fight and how to fight them. These methods can prevent your business from facing the consequences of a high chargeback rate, and protect your bottom line.

FAQ

What is a retrieval fee?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com