Chargeback Thresholds & Your Business

Table of Contents

- What are Chargeback Ratios?

- What is a 'High-Risk' Merchant?

- Chargeback Ratios for Visa

- Chargeback Ratios for MasterCard

- Chargeback Ratios for American Express

- Chargeback Ratios for Discover

- Conclusion

- Frequently Asked Questions

Preventing chargebacks isn’t just important to your bottom line. It’s vital to your company’s very existence.

That’s because chargebacks aren’t just extra expenses to deal with they’re also serious threats to your merchant accounts—the same accounts you use to process payments, do business and keep your company afloat. You see, all four major card networks have a maximum chargeback threshold for their merchants. These set stringent caps on a merchant’s chargeback ratio every month. If the merchant surpasses that cap, they can get charged additional fees, put on a warning list or even have their account shut down entirely.

You see, all four major card networks have a maximum chargeback threshold for their merchants. These set stringent caps on a merchant’s chargeback ratio every month. If the merchant surpasses that cap, they can get charged additional fees, put on a warning list or even have their account shut down entirely.

And that means no more payment processing—or profits—for you.

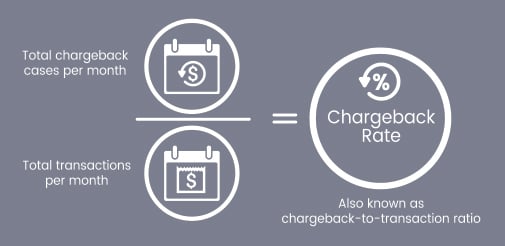

What are Chargeback Ratios?

Chargeback ratios are determined by dividing the total number of a merchant’s chargebacks per month by the total number of transactions in that same period (except MasterCard who divides the total number of merchant’s chargebacks per month by the total number of transactions in the previous month).

Here’s an example:

Say a merchant has 100 chargebacks in May and a total of 1,000 transactions. That would give them a 10 percent chargeback ratio for the month (100 divided by 1,000).

Card networks place caps on these ratios to ensure their merchants are running their businesses with integrity and that consumers are being treated fairly and satisfactorily.

Here are what these caps look like for each individual card network

What is a 'High-Risk Merchant'?

Chargeback ratios tie into the reputation and reliability of a merchant and their standing with a card network and payment processor.

High-risk doesn't denote that the merchant has done something wrong or illegal on their own. What it does signal is that the merchant is likely more prone to fraud and chargebacks;

Merchants with high fraud rates demonstrate to their card networks that they are at higher risk for losses due to fraud. This could be because they are in a higher-risk industry where fraud is more common, or it could mean that they are not putting proper fraud prevention measures in place to halt fraud from happening.

High-risk merchants could also have a lot of chargebacks, which means that they have a lot of reversed transactions. This could mean that, once again, the merchant is in a high-risk industry, or that the merchant simply doesn't work hard enough to prevent bad transactions (maybe they don't do enough to prevent fraud, or they have a high incident for bad customer service).

It's important to note on the chargeback side that it doesn't matter if the merchant is a victim of chargeback fraud. Chargebacks still count against their ratio no matter what the outcome is.

Chargeback Ratios for Visa

Visa has two different chargeback thresholds, capping its merchants at a 0.75 percent chargeback ratio and 75 total chargebacks per month.

If a merchant surpasses either of these thresholds, the network puts them on what’s called a “pre-monitoring” program, essentially sending up a red flag that something’s wrong and should be addressed. If the merchant passes 100 total chargebacks or a 1 percent chargeback ratio, they’re moved to full-scale monitoring program and considered high risk. In the event the merchant cannot lower their chargeback totals and ratio, they can be removed from the Visa network altogether.

If the merchant passes 100 total chargebacks or a 1 percent chargeback ratio, they’re moved to full-scale monitoring program and considered high risk. In the event the merchant cannot lower their chargeback totals and ratio, they can be removed from the Visa network altogether.

Chargeback Ratios for MasterCard

The MasterCard network caps merchant chargebacks at 100 per month at a chargeback ratio of 1 percent.

Like Visa, when a merchant exceeds these thresholds, they are placed on a monitoring program. If their chargeback ratio exceeds 1.5 percent for the month, the merchant is considered an “Excessive Chargeback Merchant,” and is monitored further. Failure to address surging chargebacks could result in removal from the MasterCard network.

Chargeback Ratios for American Express

The American Express network is a little different from Visa and MasterCard in that it doesn’t have hard-and-fast thresholds for chargeback ratios or totals. In order to evaluate chargeback performance, the network considers a merchant’s industry and overall risk level, total chargeback counts and chargeback ratios over time.

American Express generally wants to see merchants under 100 chargebacks per month and a chargeback ratio of under 1 percent.

Chargeback Ratios for Discover

Discover is similar to American Express in that it’s a bit more relaxed when it comes to chargeback rules.

Though it doesn’t have any specific ratio requirements or monitoring programs, the network recommends merchant keep their chargeback ratio below 1 percent and total chargebacks under 100 per month.

What’s Your Chargeback Ratio?

Having visibility into your chargebacks – specifically your ratio and total chargebacks every month – is crucial if you want to ensure the long-term health and wealth of your business.

FAQ

What is considered a high-risk business?

What is a good chargeback rate?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com