Cryptocurrency Chargebacks: What Merchants Should Know

Table of Contents

- Can You Chargeback Cryptocurrency?

- Can Cryptocurrency Prevent Chargebacks?

- Should My Business Accept Cryptocurrency?

- Will Cryptocurrency Payments Go Mainstream?

- Is Cryptocurrency Safe?

No merchant enjoys dealing with chargebacks. They drain revenue, put a merchant's account at risk, and require time and effort to properly respond to. Many e-commerce merchants are quick to welcome any new tool or strategy that can help prevent chargebacks, but there's one in particular that most merchants have been reluctant to adopt: cryptocurrency.

Most merchants see cryptocurrency as too volatile and complicated to get involved with. To be fair, accepting cryptocurrency is far from a simple task, and there are some downsides associated with accepting it. There are upsides as well, however. What do merchants need to know about cryptocurrency, how it can prevent chargebacks, and how they can decide whether accepting cryptocurrency is the right choice for their business?

Understanding how to use Bitcoin and other cryptocurrencies can be quite challenging. The technical details of how cryptocurrencies are “mined” and how the blockchain records transactions are often obtuse and complex.

Understanding how to use Bitcoin and other cryptocurrencies can be quite challenging. The technical details of how cryptocurrencies are “mined” and how the blockchain records transactions are often obtuse and complex.

Even with a strong understanding of how cryptocurrency works, implementing its acceptance on an e-commerce platform can be a daunting project.

Then there's the question of what a unit of cryptocurrency is actually worth in dollars and cents at any given moment. During the end of 2020 and the beginning of 2021, bitcoin quintupled its value in 6 months, then lost a third of that over the next two.

Bitcoin's elevator pitch is that it's a decentralized currency that can't be controlled by governments or big banks, but in practice, much of bitcoin's transaction activity is related to speculation. That means it often behaves more like a stock than a currency, fluctuating in value based on perceptions about whether the value is likely to go up or down in the future.

It's easy to see why many merchants are reluctant to do business in a currency that can change value so quickly. Nevertheless, some merchants see cryptocurrency as safer and less volatile than a payment system that allows chargebacks. That should certainly tell us something about how chargebacks are perceived, and how they are impacting merchants.

Can You Chargeback Cryptocurrency?

This is by design, as bitcoin was intended in part to function like virtual cash, where transactions are permanent and difficult or impossible to trace. This is also true of newer stablecoins, which avoid the price fluctuations caused by speculation on cryptocurrency by pinning the value to an existing currency, such as the US dollar.

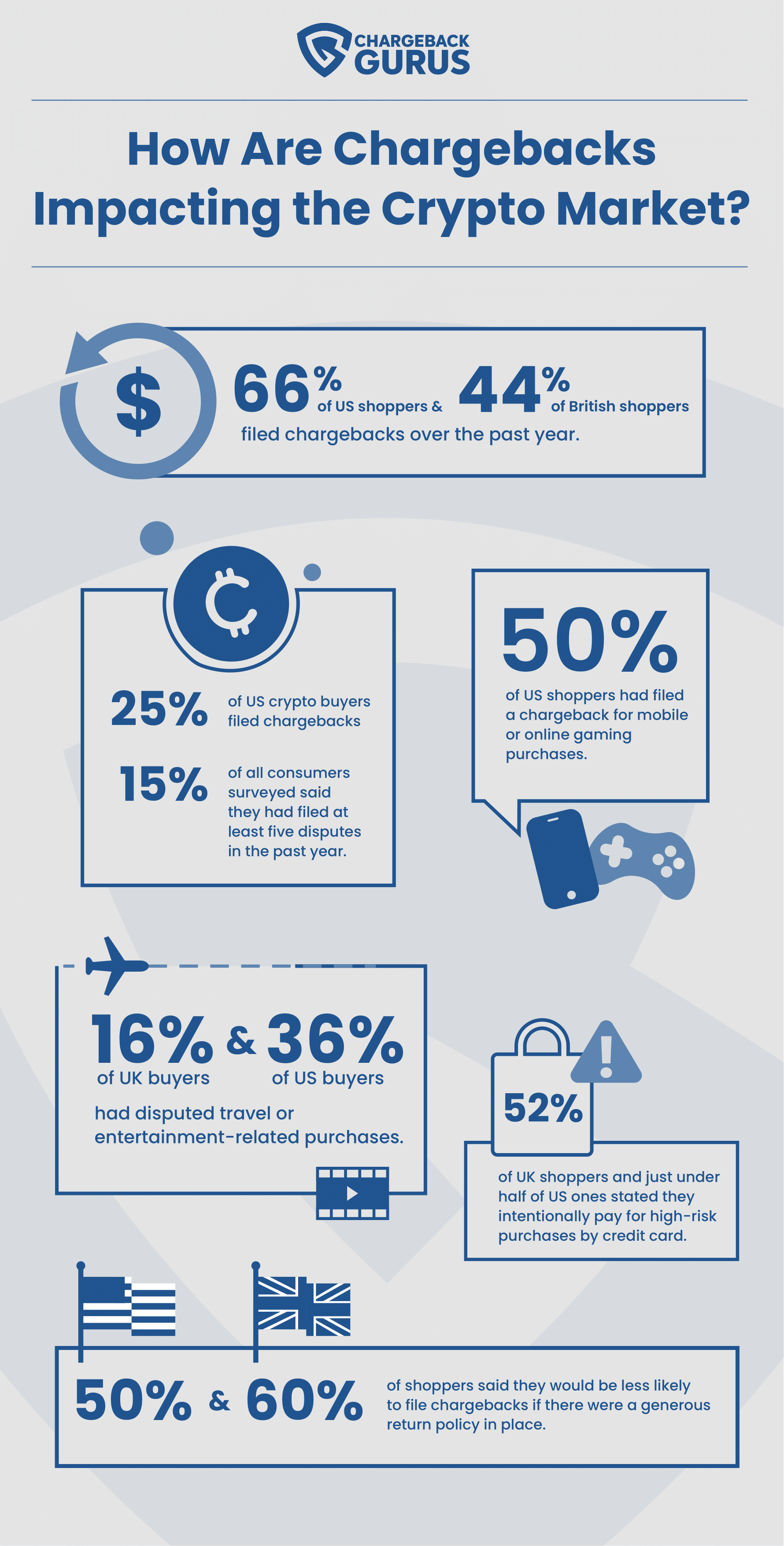

However, credit card purchases are always subject to chargebacks, and that includes purchases of cryptocurrency. For merchants selling cryptocurrency directly, this can create a problem, since the transfer of the currency is designed to be irreversible. The cost of chargebacks is high for merchants, and in this case they may lose both the cryptocurrency and the funds used to pay for it. Not to mention the chargeback fee.

In addition, some merchants are starting to accept direct credit card payments for blockchain-based assets like NFTs. These purchases are also subject to chargebacks, and present similar issues for the merchants involved. If the use of credit cards in transactions related to cryptocurrency continues to increase, it's likely that we'll see chargebacks increase as well. At the moment, cryptocurrency-related chargebacks are less common than chargebacks in other areas, but as the use of cryptocurrency in payments increases, that could change rapidly.

Can Cryptocurrency Prevent Chargebacks?

Chargebacks aren’t the only reason merchants are getting into cryptocurrencies, but with chargebacks costing businesses tens of billions of dollars each year and growing, they are undoubtedly a significant factor.

Accepting cryptocurrency payments is no longer a stunt or proof-of-concept exercise. Huge companies like Microsoft and Subway take cryptocurrency as payment, and many small businesses are following suit. JP Morgan Chase is currently implementing their own coin (JPM Coin) with the goal of making cryptocurrencies accessible to businesses of all sizes.

Most cryptocurrencies aren’t backed by any central authority like a bank or government, however.

Instead, exchanges are carried out peer-to-peer, with the blockchain serving as an objective ledger that authenticates each transaction. In this system, there’s simply no way for chargebacks to be carried out. The buyer has no bank or card network to appeal to and no way to force a reversal of the transaction. If a customer wants their money back and the transaction happened over the blockchain, they are entirely at the mercy of the merchant.

Should My Business Accept Cryptocurrency?

In addition to the lack of chargebacks, there's another benefit of conducting transactions on a peer-to-peer basis: there’s nobody in the middle collecting fees to facilitate the exchange. Payment processors take a small percentage of each debit or credit card transaction they handle, which can add up to enormous sums of money for high-volume merchants. For small businesses that operate on tight margins, these fees can take a serious cut out of their profits.

Prior to the advent of cryptocurrency, e-commerce merchants had no alternative but to accept these fees and adjust their pricing accordingly. Now that customers have more options for electronic payments, merchants may have a little more leverage.

The primary downside of accepting cryptocurrency is that merchants may want to set up a system for quickly converting it to standard currency in order to avoid the wild price fluctuations that can occur in the cryptocurrency market. Newer stablecoins avoid this problem entirely, and while their use isn't yet widespread, accepting them can put you ahead of the curve with no downside other than the time invested to modify your payment system.

Will Cryptocurrency Payments Go Mainstream?

Crypto has had some high-profile gains and setbacks recently. More and more major companies have started accepting bitcoin as payment, but Tesla stopped accepting cryptocurrency last year, citing environmental concerns.

Mining cryptocurrency and processing transactions uses a lot of electricity; Electricity which in most places comes primarily from power plants running on fossil fuels.

Mining cryptocurrency and processing transactions uses a lot of electricity; Electricity which in most places comes primarily from power plants running on fossil fuels.

In addition, speculation on Dogecoin by a relatively small online community caused the price to fluctuate wildly in a very short period of time, creating questions about how prone cryptocurrency may be to manipulation. However, Dogecoin has a much smaller market than coins like Bitcoin and Ethereum, and the larger currencies haven't shown the same level of risk so far.

Cryptocurrency isn't just attractive to a certain segment of consumers. It can be an attractive option on the merchant's side of things as well. For one thing, transaction are almost immediate. Payment card settlements can take several days to hit a merchant’s bank account, but a cryptocurrency transaction can be converted into cash via an exchange platform almost as soon as it has been completed. For merchants who struggle with cash flow issues, this can be a very attractive benefit.

Of course, once a merchant comes around to the idea that accepting cryptocurrency is a good business move, the question becomes how, exactly, to take all that Bitcoin and Ethereum that their customers are so eager to fork over. For the most part, merchants can rely on the same kind of third-party point-of-sale systems and web applications that process regular card payments.

The increasing use of cryptocurrency as a method of payment may not be without limits, however. The most popular cryptocurrencies have flaws that would prevent them from becoming a common payment method like any other. The current method of processing Bitcoin transactions, for example, has a theoretical maximum of around 7 transactions per second. By comparison, Visa processes about 1,700 transactions per second on average.

With Ethereum, a part of the transaction fee referred to as the "gas fee" increases when transaction activity is high. Between January 2021 and May 2022, the average gas fee on the Ethereum network was around $40, making it unsuitable for everyday purchases. At time of writing those fees have decreased significantly, but still hover around $10-$30. There are solutions to these issues with transaction volume, but they would require controversial changes to the fundamental rules of the currencies involved.

Is Cryptocurrency Safe?

However, we would advise merchants to be careful about some of the non-technical aspects of cryptocurrency that may not yet be on their radar, such as the tax implications and the ways in which crypto security differs from payment card security.

Fraudsters follow the money, and the more people use cryptocurrencies, the harder they’ll be working to find ways to game and exploit the system.

Cryptocurrency may circumvent the chargeback problem, but crypto alone is no solution to the underlying issues that lead to transaction disputes, such as products that don’t deliver on their promises, or customer service that isn’t responsive to customer needs.

Cryptocurrency is a powerful alternative to traditional payment methods that many customers will appreciate, but even if it was in wide enough use to supplant credit and debit cards, you’d still have to address the root causes of your disputes. If customers have no remedy for fraudulent or deceptive transactions, they may just take their business elsewhere. Eventually, market pressures may force the cryptocurrency community to introduce a chargeback mechanism into the blockchain. Merchants who were hoping for an end run around chargebacks might rage at this, but merchants who analyze and manage chargebacks properly will be able to take such changes in stride.

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com