How Visa Rapid Dispute Resolution (RDR) Prevents Chargebacks

Table of Contents

- What is Visa RDR?

- How Rapid Dispute Resolution Works

- Using Rapid Dispute Resolution Effectively

- Conclusion

It can be hard to issue a refund and say goodbye to a sale. It’s even harder when you have to write off the product you sold as well, but smart merchants know that a refund is always better than a chargeback. The problem is that once a cardholder has decided to dispute a transaction and ask for a chargeback, they’re usually done talking to the merchant.

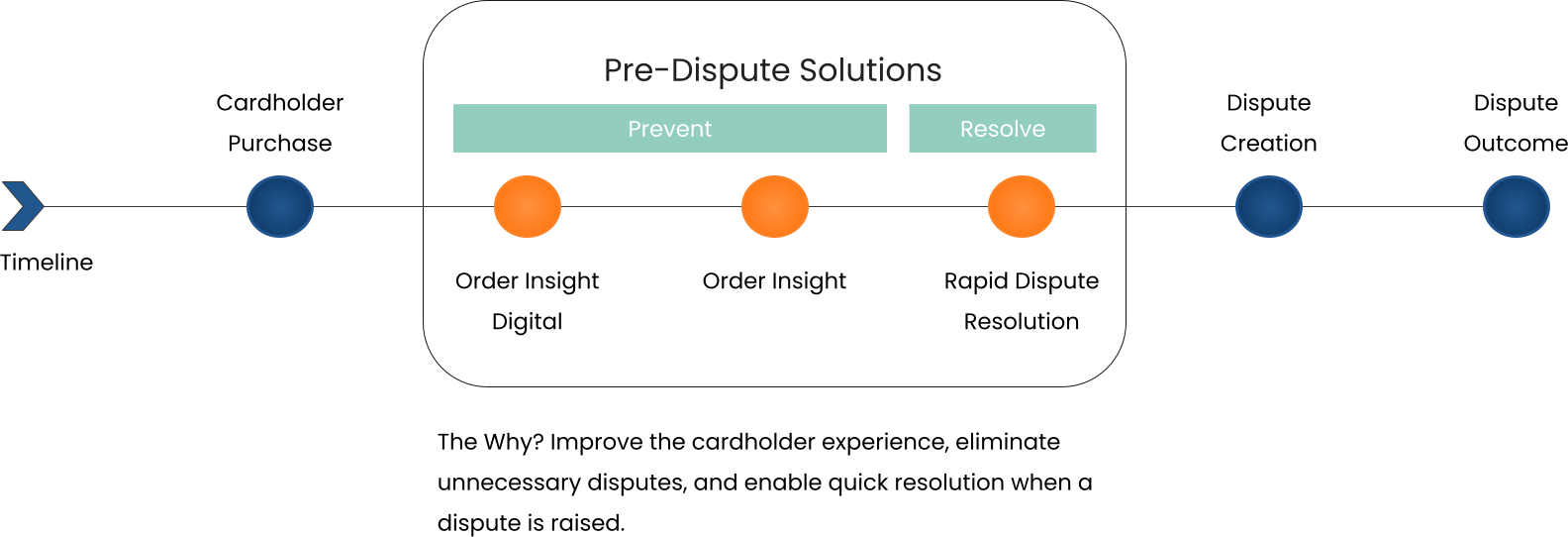

Visa’s Rapid Dispute Resolution (RDR) can provide merchants with a last-minute window of opportunity to circumvent the dispute by issuing a refund. Can merchants rely on services like RDR to stop chargebacks without hurting their revenue?

What is Visa RDR?

Rapid Dispute Resolution is a Verifi-branded pre-dispute resolution product built on the Visa network. It allows merchants to use rules-based automation to resolve eligible Visa disputes before they become chargebacks.

When eligible Visa pre-dispute cases are received that match the merchant’s rules, RDR communicates through the dispute-resolution process to accept liability and initiate a cardholder credit before the case becomes a chargeback.

Some merchants may balk at the idea of disputes triggering automatic refunds out of their merchant accounts, but remember:

- With fees and overhead included, the true cost of a chargeback can be more than double the original transaction amount

- Fighting and beating chargebacks through representment costs you, too—and victory is never guaranteed

- Every chargeback you incur raises your chargeback ratio, which can have significant negative consequences.

With these facts in mind, it makes a lot of sense to stop as many chargebacks as possible by refunding the cardholder instead.

How Rapid Dispute Resolution Works

RDR uses a merchant-defined decision engine to determine which eligible Visa pre-dispute cases should be accepted and resolved automatically. Merchants set rules that define the types of cases they are willing to resolve with a cardholder credit and the types of cases they want to allow to proceed to the chargeback phase so they can fight them through representment.

A merchant who configures RDR to credit every eligible dispute might have an impressively low chargeback rate, but they might also end up facing significant financial harm from friendly fraud.

When a merchant is enrolled in RDR, eligible Visa disputes can be routed through automated pre-dispute decisioning before they become chargebacks. RDR consults the ruleset provided by the merchant. If the case matches the merchant’s criteria for acceptance, RDR accepts liability on the merchant’s behalf and initiates a cardholder credit. If the case does not match those criteria, the case can continue into the chargeback process.

For coverage outside eligible Visa RDR cases, merchants may also use Verifi CDRN Alerts. These alerts give merchants a delayed decisioning window—typically up to 72 hours—to initiate a cardholder credit before a chargeback is filed. This distinction is important: RDR is automated decisioning for Visa pre-dispute cases, while CDRN is delayed decisioning that can extend coverage to participating Visa and non-Visa issuer cases.

Merchants can use transaction and dispute data to define their RDR decisioning strategy. Depending on the RDR implementation and decisioning method being used, relevant criteria may include information such as:

- Transaction amount

- Transaction date

- Product identifier

- Dispute category

- Chargeback reason code

- Currency code

- Authorization date and time

- Issuer’s bank identification number

An “accept” response results in the acquirer sending an immediate credit to the issuer. A “decline” response allows the dispute to proceed to the chargeback phase.

When RDR initiates an automatic refund with the merchant’s acquiring bank, merchants are protected by Visa’s guarantee that the dispute has been resolved and no chargeback will follow.

RDR Data Flow

The full RDR process works as follows:

- Transaction Inquiry request with search criteria to find the transaction

- Transaction summary information based upon search criteria

- Issuer selects dispute category (Fraud, Authorization, Consumer, or Processing)

- Visa returns ATR flag = 'TRUE' indicating OI details are available for review

- Issuer makes ATR request to retrieve OI details when seller is participating

- VROL communicates with Verifi to retrieve OI details when seller is participating

- ATR response enhanced to include additional purchase details for review

- Issuer reviews associated transaction and additional purchase details with cardholder to further triage the dispute

- If cardholder wants to pursue a dispute, issuer submits dispute questionnaire

- If transaction is eligible for RDR; Verifi applies seller-defined rules to auto-decision seller response to request for credit

- VROL returns response indicating successful questionnaire submission

- VROL routes dispute questionnaire and TC15 to acquirer, acquirer withdraws funds from seller

- Standard funds clearing and settlement

Using Rapid Dispute Resolution Effectively

The best way for merchants to use RDR is to decide ahead of time what kind of chargebacks they want to invest time and labor into fighting through representment. True fraud and merchant error chargebacks that have a legitimate basis cannot be fought effectively; it’s much better for merchants to refund these chargebacks and avoid them. That leaves only friendly fraud chargebacks—chargebacks that have no legitimate basis, whether the cardholder understands that or not.

Friendly fraud always masquerades as true fraud or merchant error, since the cardholder will have to provide some plausible reason for wanting the chargeback. For each merchant, the particular circumstances and indicators of illegitimate chargebacks will be different. Some merchants may have high chargebacks associated with a particular product; others may find that customers from a particular region give them the most trouble.

By analyzing their chargebacks, merchants observe patterns in the data that show which chargebacks they should prevent with refunds and which ones they should choose to fight.

For example, you could choose to refund all disputes under $100 simply because it isn’t worth your time to represent those. Or, you might find that you have a high rate of success fighting chargebacks carrying a particular reason code, so you arrange the rules to allow all disputes with that code to proceed.

Merchants must also remember to reconcile their bank statements against the activity generated by RDR, much as they would do with chargebacks. Finally, they must also regularly analyze their RDR data to see if the rules are generating desirable outcomes and positive ROI.

You need to know if RDR is handing out refunds to friendly fraudsters, or if it is defeating its own purpose by allowing too many unwinnable chargebacks to go through. Only by reporting and analyzing RDR data can you determine whether you’re truly using it effectively.

Conclusion

Rapid Dispute Resolution can be a powerful tool for avoiding chargebacks, but merchants must use it with caution, developing and refining their ruleset with a careful, data-driven approach that closely monitors ROI and chargeback activity. As a set-it-and-forget-it solution, RDR has the potential to get merchants into trouble—friendly fraudsters really do share tips about which merchants are the easiest to scam.

Once you've gotten RDR up and running, you should carefully monitor your refund rate. Seeing a higher rate of refunds with RDR is a normal part of preventing chargebacks, but if your refund rate is skyrocketing beyond what you're comfortable with, you may want to reexamine your ruleset.

If you're close to exceeding Visa's chargeback thresholds or have already exceeded them and are looking to drop back down below the line, however, it may be worth re-calibrating your comfort zone. Oftentimes the consequences of excessive chargebacks can be far greater than the consequences of issuing a lot of refunds.

For many merchants, consultation with an experienced chargeback management company may be the best way to implement RDR. A chargeback management company will take a careful look at all your available data and your business goals to carefully craft the ideal ruleset to implement with RDR, customized to your individual needs.

RDR is also just one small part of a comprehensive chargeback defense strategy that should address your vulnerabilities at every point in the process. RDR can provide a valuable off-ramp for an escalating dispute, but it’s still better to fix the root causes that generate disputes in the first place.