How to Reconcile Chargebacks and Chargeback Reversals

Table of Contents

- What is Chargeback Accounting?

- How Can You Understand The Major Banks?

- What are the Independent Sales Organizations?

- Should I Have Reserve Funds?

- Keep a Close Eye on Your Statements

- Conclusion

- Frequently Asked Questions

Dealing with chargebacks and the process of fighting them can be a real headache, so it can be a relief to get to the end of a month and know that once you've reconciled the debits and credits associated with a chargeback to your bank statement, you'll never have to see it again.

However, chargeback accounting can be tricky at times, depending on what type of merchant account you have. Different banks and payment processors have different ways of handling chargeback debits and credits.

In order to keep your books clean and accurately record how your finances have been affected by chargebacks, you need to know how the entities you're dealing with will present them to you on your monthly statements.

What is chargeback accounting?

Normal accounting of transactions is something every merchant is familiar with. When you start factoring in chargebacks, however, you'll start running into problems with cash flow and revenue if you don't balance your books right.

Some of the challenges that come with chargeback accounting include:

Time

Chargeback disputes take time. The cardholder may not enact a dispute right away, so you may find yourself with a reversal of a transaction that's on last month's books. Once you receive word of the chargeback, you may want to put forward a dispute of your own, which can take further weeks or months to resolve. Altogether, you can easily end up having to track and account for a single transaction across three months or more.

Overlapping expenses

When a chargeback occurs, there are several expenses you'll need to keep track of. The chargeback fee is the most obvious one, but you may also have to account for things like the transaction fee you still have to pay when the charge is reversed, or the cost of any merchandise sold to the customer.

Chargebacks also come with hidden costs such as customer service and acquisition. While these costs might not throw off your accounting, you may want to include them if you want an accurate picture of how much chargebacks are costing you.

Multiple transactions

The various costs and fees associated with a chargeback will usually be spread out over multiple transactions. If you want to have a good idea of the total cost to your business, you'll need to sift these out from among the many other transactions your business is conducting.

How do banks account for chargebacks?

How your individual business needs to handle chargeback accounting may hinge on whether you obtained your merchant account from an agent, an aggregator, or directly from a bank.

How your individual business needs to handle chargeback accounting may hinge on whether you obtained your merchant account from an agent, an aggregator, or directly from a bank.

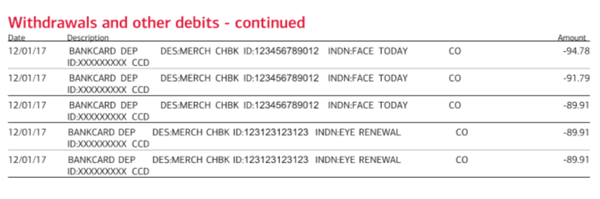

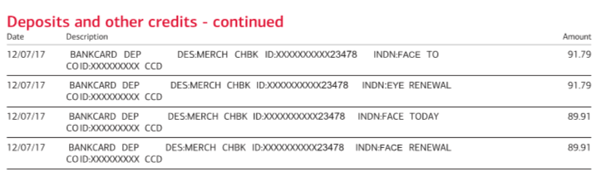

Most major banks, including Chase, Wells Fargo, and Capital One, offer merchant accounts directly to those who qualify. These banks also make some efforts to simplify chargeback accounting for their customers.

When they send you your account statement at the end of the month, you'll find each of your chargebacks listed as individual line items, with the transaction amount and the chargeback fee split out as separate amounts. The same goes for chargeback reversals.

These banks make it easy to identify fees and transaction amounts for reconciliation purposes. The samples below provide a general idea of what you might see when looking at chargebacks in your account.

Each amount will be categorized separately on your statement. However, the statement is the only notification you will receive of chargeback-related withdrawals or deposits to your account.

What are independent sales organizations?

ISOs (also known as Merchant Service Providers) are third-party merchant account providers that often service smaller or higher-risk merchants.

The statements you get from them will have line items showing your chargebacks, but some ISOs lump the fees and transaction amounts together in a single line.

While this can make it a bit easier to account for the total cost of a chargeback, it can make it challenging to trace a chargeback line item back to the original transaction that spawned it, since the amounts will be different. Remember that you always have the right to contact your ISO to ask for an explanation of any chargeback line items, along with a breakdown of the fees it includes.

Chargebacks and reserve funds

Some banks don't include chargeback or reversal fees in the amounts listed on your statement. In these cases, you will see only the disputed amount.

The reason for this is that they are  holding fees related to chargebacks, representment, and reversals in a reserve fund. They may hold them there for up to six months before releasing them to you. This can make things confusing when you are trying to ascertain the total financial impact of a chargeback.

holding fees related to chargebacks, representment, and reversals in a reserve fund. They may hold them there for up to six months before releasing them to you. This can make things confusing when you are trying to ascertain the total financial impact of a chargeback.

You may also find yourself receiving credits to your account that you can't easily or immediately identify, because they are related to months-old chargeback reversals.

When you're confused, it's best to reach out to your bank for an explanation before accounting discrepancies carry over from month to month and spiral out of control. You always have the right to know how fees are calculated and how each charge on your statement breaks down

Keep a close eye on your statements

Keeping your accountants and bookkeepers happy isn't the only reason to pore over your bank statements. It's important to compare statements to your own chargeback records to make sure you're being charged—or credited—correctly.

It's tempting to trust our banks to be so automated and precise that we don't have to worry about inaccuracies, but mistakes can and do happen.

Any given chargeback can be a confusing, multi-step process, with many opportunities for human error.

Fees can be calculated incorrectly and reversals can be missed. While much of this accounting is automated these days, computers can make mistakes, too. It's not at all unheard of for a glitch in a bank's systems to cause the same fee to be assessed twice, for example. Plus, even if the calculations are always done correctly, they can still end up being wrong if the original information they were based on was incorrect.

When participating in chargeback representment, keep your own notes about how much you expect to get back. Track your charges and compare statements to your notes to ensure you're getting the right amounts credited back to you.

If a charge doesn't look right, don't just assume the bank knows better than you. Call them up and ask them to walk you through it until you understand and agree with how they arrived at the number they did. Even when you have a trusted bank that's looking out for you, you have to be your own best advocate, especially when you're deep in the confusing and complicated world of chargebacks.

FAQ

How should you record a chargeback?

Is a chargeback an operating expense?

Is a chargeback a refund?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com