Chargeback Prevention Alerts | 2025 FAQ

Table of Contents

- What Are Chargeback Prevention Alerts?

- How Do Chargeback Prevention Alerts Work?

- How Much Do Chargeback Alerts Cost?

- What Are the Benefits of Chargeback Prevention Alerts?

- Who Are the Major Providers of Chargeback Alerts?

- What Percentage of Chargebacks Can Be Prevented by Alerts?

- What Do I Need to Get Started with a Chargeback Prevention Alert Network?

- How Long Does It Take to Set Up Chargeback Prevention Alerts?

- What Are Fully Managed Alerts

- Should I Let a Chargeback Management Company Handle Chargeback Alerts for Me?

- Are Chargeback Alerts the Best Way to Prevent Chargebacks?

- What Happens If I Get Too Many Chargebacks?

- What Is a High-Risk Merchant?

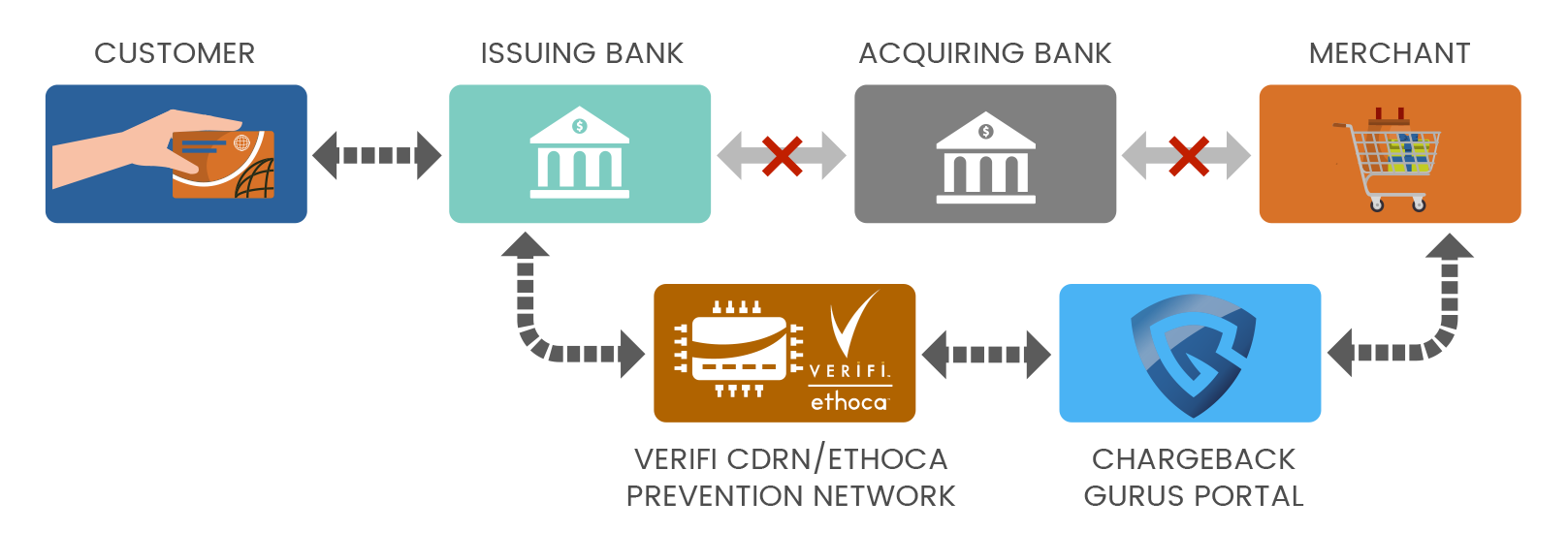

What Are Chargeback Prevention Alerts?

During the chargeback process, the cardholder typically works with their issuing bank, and the merchant never knows about the dispute until they are notified about the chargeback after the fact.

But with a chargeback alert, you can get a notification of a pending chargeback in progress. If you choose, you can issue a refund in response to avoid the chargeback.

How Do Chargeback Prevention Alerts Work?

If the merchant believes the request is invalid, they can always opt to let the process play out and dispute the chargeback.

How Much Do Chargeback Alerts Cost?

What Are the Benefits of Chargeback Prevention Alerts?

Merchants have to pay fees for chargeback prevention alerts, but in the long term, paying those fees can be a lot more cost-effective than dealing with the expenses and lost revenue associated with being enrolled in excessive chargeback programs or having your account suspended or terminated.

Who Are the Major Providers of Chargeback Alerts?

What Percentage of Chargebacks Can Be Prevented by Alerts?

The percent of chargebacks prevented by alerts will vary based on:

- Transaction Count (The more transactions, the better the coverage)

- Customer Bank Location (US customer base has better coverage than overseas)

- Years in Business (Established businesses can have better coverage than new merchants)

Here are some estimates based on our own internal data analysis:

|

Service/Product |

Verifi |

Ethoca |

|

Physical Goods |

21% |

17% |

|

Digital Goods |

41% |

30% |

|

Digital Service |

17% |

33% |

|

Subscription Industry |

19% |

14% |

What Do I Need to Get Started with a Chargeback Prevention Alert Network?

To get your merchant accounts enrolled in the prevention alert network, you need to provide the following information:

- Merchant/business name

- Business registered address

- Billing descriptor (Name as it appears on customer credit card statement)

- Merchant account number (The ID provided by your payment processor)

- Access to your sales system (To issue refunds and resolve the alerts)

How Long Does It Take to Set Up Chargeback Prevention Alerts?

- New Merchant: 45 – 60 days (Haven’t processed any transactions before)

- New Customer: 20 – 30 days (Never enrolled in a prevention alert network before)

- Existing Customer: No delay (Previously enrolled in prevention alerts, but switching providers)

What Are Fully Managed Alerts?

Fully managed alerts are a hands-off solution for merchants who want better control over chargebacks without the workload of monitoring and responding to alerts themselves. With this service, every step—from receiving the alert to deciding on a resolution—is handled by a dedicated team.

Unlike standard alert systems that rely entirely on automation, fully managed alerts include expert oversight on top of automated systems. These specialists catch edge cases that software might miss, such as partial disputes or transactions with inconsistent data. This level of review increases interception rates and minimizes disputes slip through.

Merchants also benefit from customizable alert settings. You can disable specific types of alerts that aren’t delivering value, helping to cut unnecessary costs.

Alerts are not only configurable by type but also by strategy—blanket refunds aren’t required. Instead, custom responses can be applied based on transaction details, risk level, or customer behavior.

This service includes built-in cost protections, such as zero charges for eligible duplicate alerts. Automated monitoring tracks the chargeback ratio on each MID (Merchant ID), and notifies you when thresholds are close, allowing time to act before penalties kick in.

For high-risk merchants or businesses dealing with complex disputes, fully managed alerts provide a practical way to keep chargebacks under control without losing time or visibility.

Should I Let a Chargeback Management Company Handle Chargeback Alerts for Me?

What Happens If I Get Too Many Chargebacks?

Businesses labeled as high high risk are typically enrolled in dispute mitigation programs that may impose additional fees for chargebacks. If a merchant remains in such a program for too long, large monthly fees may be added, and the merchant's acquirer may choose to terminate the merchant account.

Chargeback alerts can be expensive, but for merchants in high-risk industries or those in danger of exceeding a 0.9% chargeback ratio, the cost is well worth it. In most cases, however, alerts should be used in combination with other methods such as representment and root cause analysis.

What Is a High-Risk Merchant?

When a merchant operates in a high-risk industry or has too many incidents of fraud or chargebacks, they can be labeled as high risk. High-risk merchants may have limits placed on their accounts, and they may be enrolled in monitoring programs by card networks.

Consequences of being labeled high risk can include limits on monthly processing volume, holding reserve funds (to protect themselves from loss), and possibly even termination of the merchant account.

If a merchant has been designated as high risk due to a high chargeback ratio rather than because of the industry they operate in, this high risk status can be removed by maintaining a chargeback ratio below the threshold for a few months.