Visa Claims Resolution (VCR) & What It Means For Merchants

Table of Contents

- What is Visa Claims Resolution?

- What chargeback terminology did Visa change with VCR?

- The Visa Claims Resolution dispute process

- What is VCR Allocation?

- What is VCR Collaboration?

- How does Visa Claims Resolution affect merchants?

- What happens if you don't acknowledge a chargeback dispute?

- Can the acquirer acknowledge chargeback disputes on behalf of a merchant?

- What do I have to do to ensure I am in compliance with VCR?

In order to improve their processes, reduce fraud, and address any loopholes or abuses of their systems they discover, all the major card networks make frequent updates to their rules and policies. Most of these changes are fairly minor, but every once in a while a change comes along that really shakes things up. The EMV liability shift is one example of this.

The Visa Claims Resolution (VCR) initiative is another. What is Visa Claims Resolution, what changes did it make, and how did those changes affect merchants?

What is Visa Claims Resolution?

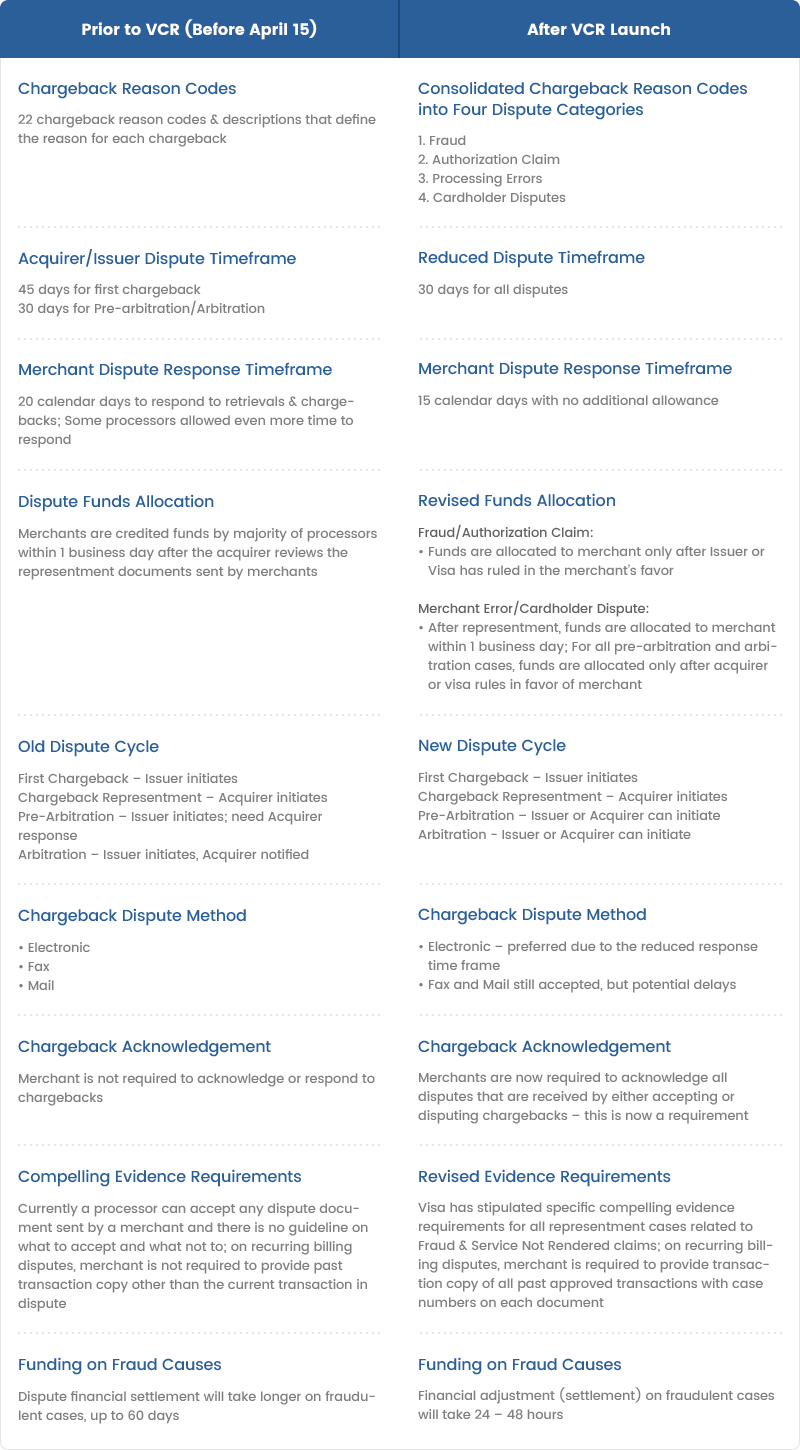

What chargeback terminology did Visa change with VCR?

Visa also overhauled its system of chargeback reason codes. The new codes, which can be found in our reason code guide, start with a two-digit number indicating which of Visa's four dispute categories it falls into:

- 10 — Fraud

- 11 — Authorization

- 12 — Processing Errors

- 13 — Consumer Disputes

The Visa Claims Resolution dispute process

Visa made several changes to the dispute process. With Visa Claims Resolution, the dispute process is now split into two different workflows. Which workflow a chargeback goes through depends on the dispute category for the chargeback.

Fraud and Authorization disputes will follow the Allocation workflow, while Processing Errors and Consumer Disputes will follow the Collaboration workflow.

What is VCR Allocation?

Disputes that Visa determines to be invalid will have their liability assigned to the issuing bank. If a dispute is considered valid, the merchant can still contest it. However, rather than representment, (or a dispute response, as Visa now calls it), the merchant will be initiating pre-arbitration.

What is VCR Collaboration?

This process is largely the same as it was before, but issuers will now have to fill out a form providing greater detail about the dispute before initiating the process.

Visa has also tightened the deadlines for both merchants and issuers. Here's a rundown of all the changes in detail:

How does Visa Claims Resolution affect merchants?

For Fraud and Authorization disputes, merchants now experience a faster and more automatic dispute process. Issuing banks are also now incentivized to conduct a more thorough investigation of cardholder claims before filing a chargeback.

For Fraud and Authorization disputes, merchants now experience a faster and more automatic dispute process. Issuing banks are also now incentivized to conduct a more thorough investigation of cardholder claims before filing a chargeback.

This makes the process more focused on resolving disputes without Visa getting involved through arbitration. Once a dispute enters arbitration, merchants and cardholders must accept Visa's decision. With the new process, a chargeback is more likely to be resolved before that happens.

FAQ

What happens if you don't acknowledge a chargeback dispute?

Can the acquirer acknowledge chargeback disputes on behalf of a merchant?

What do I have to do to ensure I am in compliance with VCR?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com