Visa Merchant Purchase Inquiry VMPI Frequently Asked Questions - 2023

Table of Contents

- What is Visa Merchant Purchase Inquiry (VMPI)?

- How does Visa Merchant Purchase Inquiry (VMPI) work?

- What is Visa Resolve Online (VROL)?

- What alerts does Visa Merchant Purchase Inquiry (VMPI) provide?

- How effective is Visa Merchant Purchase Inquiry (VMPI)?

- Can VMPI prevent all my chargebacks?

- How do I get started with Visa Merchant Purchase Inquiry (VMPI)?

- What is a certified VMPI Facilitator?

- What can a certified Visa Merchant Purchase Inquiry (VMPI) Facilitator offer me?

- How can I make the best use of Visa Merchant Purchase Inquiry (VMPI)?

- The bottom line on VMPI

- Do I need Visa Merchant Purchase Inquiry (VMPI)?

- What is a merchant purchase terminal?

- What is a merchant account?

The odds are pretty good that the next credit card transaction your online store processes will be a Visa card. With over 335 million cards in circulation, accounting for more than half of all credit cards worldwide, Visa’s reach and influence cannot be overstated.

To keep their position at the top, Visa makes every effort to stay at the forefront of the payments industry, updating their policies and adopting new technologies and systems frequently to adapt to the changing world of commerce. One of those new systems was the Visa Merchant Purchase Inquiry Program, or VMPI.

In 2020, after Visa acquired Verifi, Visa merged the VMPI system with Order Insight, a similar system created by Verifi. Visa decided to use the Order Insight name for the new version. While we have an article going in-depth on Order Insight, this article covers the details of the VMPI program and has been updated with information about how the new version under Order Insight differs.

What is Visa Merchant Purchase Inquiry (VMPI)?

VMPI offers merchants a chance to see and respond to cardholder questions about unrecognized transactions before they have a chance to become chargebacks.

With chargeback rates in eCommerce at record levels and banks making it easier than ever for cardholders to dispute their purchases, VMPI is a powerful tool for merchants who want to minimize chargebacks and hold on to their revenue.

How does Visa Merchant Purchase Inquiry (VMPI) work?

According to information provided by Visa, around 3 million chargebacks each year are initiated because the cardholder was looking at their account information online and saw a transaction they didn’t recognize. While in some cases this may be due to true fraud, more often the cardholder either forgot about the transaction or doesn’t associate the merchant descriptor attached to the charge with the business they made a purchase from.

According to information provided by Visa, around 3 million chargebacks each year are initiated because the cardholder was looking at their account information online and saw a transaction they didn’t recognize. While in some cases this may be due to true fraud, more often the cardholder either forgot about the transaction or doesn’t associate the merchant descriptor attached to the charge with the business they made a purchase from.

Normally, when a cardholder calls their bank to report an unrecognized transaction, there are few barriers in place to stop their concerns from turning into a chargeback. Cardholders who speak with human customer service representatives at their bank may be asked questions or provided with prompts from their transaction history that may help them recall making a legitimate but unrecognized transaction, but it’s increasingly common for cardholders to make these reports through automated online systems.

While originally VMPI only worked when the cardholder called the bank, the new Order Insight version can be integrated with the bank's existing online and mobile systems for cardholder disputes.

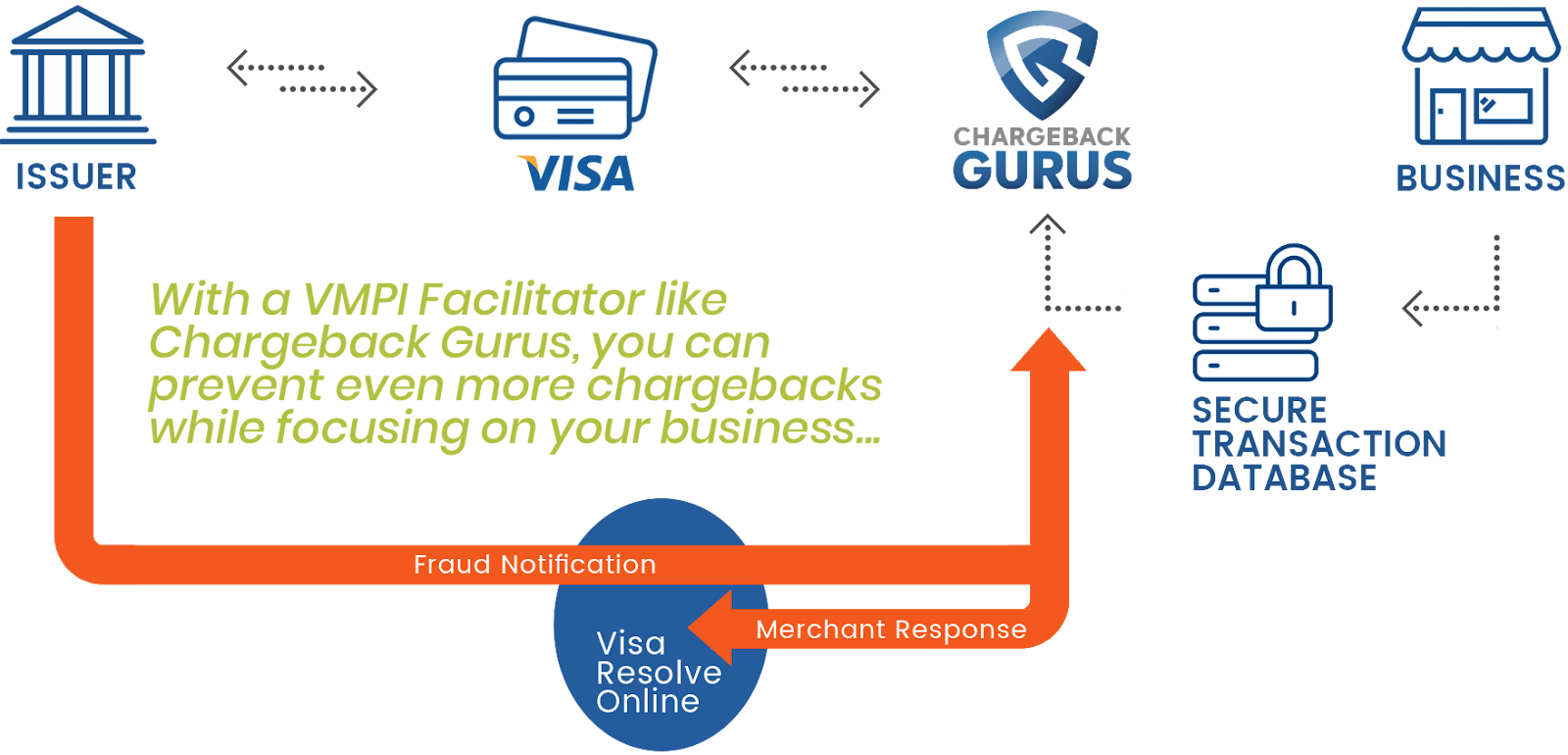

Issuing banks can investigate these disputes through the Visa Resolve Online (VROL) system to get more information about the transaction through the Visa network. However, information received in this way does not in any way guarantee that the cardholder will recognize the transaction and withdraw their dispute.

When a dispute reaches VROL, Visa will check to see if the merchant involved has chosen to implement VMPI. If they have, they will send an electronic message with information about the transaction to the merchant.

At that point, the merchant has the opportunity to identify the transaction and respond in real time with data and documentation that can either jog the cardholder’s memory or prove to the bank that the transaction is legitimate. Visa then shares that information with the issuing bank, which shares it in turn with the cardholder.

Most of the time, the information provided by the merchant will be sufficient to help them remember making the transaction, stopping them from pursuing a chargeback.

Merchants can provide product information, shipping and delivery confirmation, correspondence, signatures, and other documentary evidence — the same kind of evidence they’d use to fight an actual chargeback in representment.

Even “friendly fraudsters” who knowingly dispute legitimate transactions will often back down in the face of incontrovertible evidence that they were well aware of the purchase they were making.

Best of all, even if the unrecognized transaction wasn’t valid, the merchant can still prevent a chargeback. They can instead choose to refund the customer’s money as part of their VMPI response, effectively ending the dispute before it becomes a chargeback. For merchants who are in danger of exceeding their chargeback threshold (or who simply want to avoid costly chargeback fees), this is an incredibly helpful option.

What is Visa Resolve Online (VROL)?

- Transaction inquiries can be used to quickly retrieve transaction information.

- Dispute questionnaires help you gather relevant information from cardholders.

- Financial processing enables you to process financial transactions corresponding to chargebacks, representments, adjustments, and miscellaneous fees.

VROL was created as part of the Visa Claims Resolution initiative in 2017, which was intended to decrease the time it takes to resolve a chargeback by streamlining the dispute process and stopping many invalid chargebacks from progressing beyond the first stages of a dispute.

What alerts does Visa Merchant Purchase Inquiry (VMPI) provide?

It’s not at all uncommon for a transaction to include multiple alerts. For instance, you might see an inquiry followed by notifications for “stop payment” and “deflected” all in a single transaction. (The “deflected” notification indicates that a chargeback has been prevented.

How effective is Visa Merchant Purchase Inquiry (VMPI)?

Can VMPI prevent all my chargebacks?

We encourage all eligible merchants to incorporate VMPI as one part of their overall chargeback management strategy.

How do I get started with Visa Merchant Purchase Inquiry (VMPI)?

The primary advantage of using a facilitator is that you’ll get up and running with VMPI much faster.

The wait time with Visa and the process involved to get approved from Visa is usually longer and businesses prefer to work with a facilitator rather than working with Visa.

Aside from getting you started faster and enabling you to start using VMPI right away, another benefit of using a facilitator is that they can make integrations with your existing systems much more easily and can provide you with analytics to better evaluate the effectiveness of the VMPI program.

To get started with VMPI, you’ll need to provide your Card Acceptor ID as well as your acquirer’s Bank Identification Number. The facilitator will also need you to upload all of your order and transaction information to a secure server every day, either via SFTP or with API integration.

These daily uploads should include at least the following information for each purchase, depending on your industry and type of business:

- Cardholder name

- Order date

- Billing address

- Shipping address

- Product or service purchased

- Delivery status

- Tracking number

- Refund status and information

The more information provided, the better. Thorough, detailed information helps the issuing banks make the right decision.

What is a certified VMPI Facilitator?

How long does it take to get started with Visa Merchant Purchase Inquiry (VMPI)?

With a facilitator’s assistance, it can take up to two weeks to go live with VMPI. Here are the steps in the process, along with their estimated time frames:

- Gathering Visa Card Acceptor ID and Acquirer Bin Info: 1 – 3 Business Days

- Data Integration with Chargeback Gurus: 1 – 3 Weeks

- Visa Acceptance Time Frame: 1 – 2 Weeks

- Go-Live Testing: 1 – 2 Business Days

What can a certified Visa Merchant Purchase Inquiry (VMPI) Facilitator offer me?

Be sure your facilitator provides in-depth reports to keep track of what VMPI is actually doing. In order to help our clients monitor the effectiveness of VMPI, Chargeback Gurus provides a dashboard for alert monitoring, which shows the number of alerts issued by Visa, how many were prevented from becoming chargebacks, and how many become chargebacks despite VMPI.

How much does a certified Visa Merchant Purchase Inquiry (VMPI) Facilitator cost?

The cost of VMPI facilitation will vary depending on the volume of transactions — the higher the volume, the lower the cost per transaction.

The cost of VMPI alerts can range from $8.00/Alert to $10.00/Alert. Schedule a meeting and consult an expert from the Gurus team to learn more.

How can I make the best use of Visa Merchant Purchase Inquiry (VMPI)?

You don’t want to treat VMPI as a set-it-and-forget-it solution, however. With revenue and chargebacks on the line, VMPI should be carefully monitored by actual humans in order to ensure that all inquiries are addressed swiftly and appropriately:

VMPI as a set-it-and-forget-it solution, however. With revenue and chargebacks on the line, VMPI should be carefully monitored by actual humans in order to ensure that all inquiries are addressed swiftly and appropriately:

Merchants should also take advantage of the information and opportunities afforded them by VMPI. Every communication you receive is a learning experience and a chance to avoid future disputes.

For example, you may find that customers are confused by the name your business appears under on their credit card statement. It’s not uncommon for a merchant to incorporate under one name, do business under a different name, and for customers to see the first name (which they don’t recognize) on their credit card statement because the merchant never updated that information. This is an easy thing to fix!

If you get a VMPI query from a known customer you have dealt with in the past — who can be reasonably expected to remember the purchase they made — you may have a friendly fraudster on your hands. It may be prudent to block that customer from purchasing from you in the future, and cancel any outstanding or recurring orders they may have placed.

The bottom line on VMPI

Visa has given merchants a great tool with VMPI, which has the potential to save considerable amounts of money for merchants who deal with a high volume of disputes and chargebacks. VMPI creates a space and opportunity for merchants to respond to disputes before they become chargebacks, allowing them to avoid fees, correct fixable problems, and defend against fraudsters who dispute charges under false premises.

For merchants who really want to improve and optimize their business operations, VMPI also provides useful information about customer behavior and attitudes and can highlight potential problems with the merchant’s procedures. Merchants who are willing to apply the right analytics to the data they can glean from VMPI will find that there is much to be learned from customers who try to dispute their charges.

VMPI is a vital part of a merchant’s overall chargeback defense strategy and Chargeback Gurus is a certified VMPI Facilitator. So if VMPI seems like too much work to take on — yet another always-on communications channel for the harried business operator to monitor and address — remember that you can get started with VMPI through Chargeback Gurus at any time.

FAQ

Do I need Visa Merchant Purchase Inquiry (VMPI)?

What is a merchant purchase terminal?

What is a merchant account?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com