What is Visa Merchant Purchase Inquiry Program (VMPI)?

Table of Contents

- What is Visa Merchant Purchase Inquiry (VMPI)?

- What is the purpose of VMPI?

- What is the VMPI Process?

- Can VMPI Prevent Chargebacks Completely?

- Can VMPI Reduce the Need for Prevention Alerts?

- Pros & Cons of Using VMPI

- The Unknowns in VMPI

- Who is VMPI for?

- How Do Merchants Sign Up for VMPI?

- Conclusion

- Frequently Asked Questions

The Visa Merchant Purchase Inquiry program, also known as VMPI, was introduced by Visa in 2017.

Visa Merchant Purchase Inquiry (VMPI) enables Visa merchants to respond to card holder transactions that are not recognized, and other potential disputes, by providing relevant order information in close to real-time to the issuing banks.

Ready to find out more about VMPI? This comprehensive guide should help.

What is Visa Merchant Purchase Inquiry (VMPI)?

VMPI is a process to help merchants respond to customer disputes before they become chargebacks.

VMPI is a process to help merchants respond to customer disputes before they become chargebacks.

When a cardholder disputes a transaction, they have one of two places to go: you, or their bank.

If they come to you, and you are receptive to their issue (whether it is poor customer service, fraud, confusion about a bill item, or some other issue), then you can issue a refund. While you may be out a purchase, you served a customer and avoided a chargeback.

If the customer goes to their bank, however, then they can get a transaction reversed. As a merchant, you have no control over the process, no input, and no say in what happens. Once the issuing bank agrees to the chargeback, the money is taken from your bank account unless you can demonstrate that it was legitimate through representment.

The problem is that a chargeback counts against you even if you win. You chargeback ratio is still affected, which means that your merchant account and standing with the network could still be impacted.

VMPI is a program offered by VISA to help merchants. With it, merchants can receive a notification alert about a pending chargeback with a request for more information. If the information you provide can demonstrate that the transaction was legit, then the bank can use that info to deny the chargeback request and save you a chargeback on your record.

What is the Purpose of VMPI?

In 2015, Visa identified over 2.6 million chargebacks that were initiated because cardholders did not recognize the transactions. This is an increase of over 13% from the prior year. In addition, 20% of all chargebacks were tied to purchases of digital goods, which includes electronic downloads of movies, music and phone application purchases.

As the number of transactions related to digital goods continues to increase, so does the potential for an increased number of disputes. Managing the dispute and trying to resolve it has been expensive for the issuers, merchants, and the card networks as well.

Hence VMPI was introduced to the Card-not-Present community, with the sole goal to connect issuers and merchants and reduce disputes that aren't really disputes.

What is the VMPI Process?

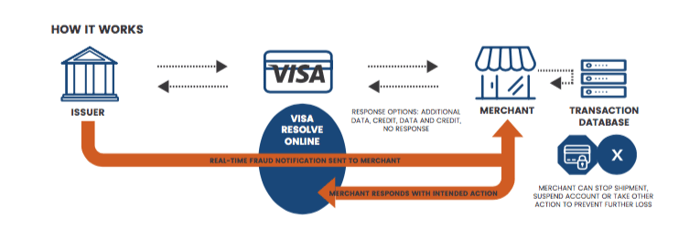

merchants’ transaction database and the issuing banks through Visa’s engine.

merchants’ transaction database and the issuing banks through Visa’s engine.The process allows merchants to seamlessly share information through VROL to the issuing banks, and involves the following steps:

- Cardholder contacts their issuing bank about a transaction they may dispute. Issuer retrieves transaction information from Visa Resolution Online (VROL)

- Visa identifies if the merchant participates in Visa Merchant Purchase Inquiry (VMPI) program

- Visa engine sends a notification to the merchant requesting for information pertaining to the transaction in dispute

- Merchant identifies transaction and pulls key data elements such as order information, tracking information, refund information, etc.

- Merchant responds through VROL in near-real-time to the issuer

- Visa shares enhanced data with issuer, who then uses the data with the cardholder

Can VMPI Prevent Chargebacks Completely?

The sole purpose of VMPI is to provide more visibility to issuing banks pertaining to the card holder transaction.

Even if the merchant provides the transaction data to the issuing bank, there is no guarantee that it can prevent a chargeback.

The issuer might convey the purchase information to the card holder and the card holder might still deny the transaction and opt for a chargeback. We can anticipate a reduction in chargebacks to a certain degree, but it cannot eliminate them completely.

Can VMPI Reduce the Need for Prevention Alerts?

The Prevention Alert Networks do not have coverage from all issuing banks. Hence, they are not able to intercept all the chargebacks. This is one of the drawbacks of prevention alerts. The advantage of prevention alerts, however, is that the merchant has the flexibility to issue a refund and prevent a dispute from happening in the first place.

In contrast, VMPI does not provide the flexibility to issue refunds to the alert notifications received from the issuing bank. It ONLY acts as an engine to provide transaction visibility.

Hence, merchants with high chargeback thresholds might still use Prevention Alerts along with VMPI.

Merchants who participated in the VMPI program were able to prevent up to 60% of visa disputes. Also merchants who continued to use VMPI along with Prevention Alerts were able to proactively prevent disputes from other card brands as well.

VMPI has become more effective in preventing chargebacks and the need for Prevention Alerts is decreasing among merchants who face less than 1% chargeback ratio. But merchants exceeding the 1% chargeback threshold still utilize both VMPI and Prevention Alerts to maximize their chargeback prevention.

Pros & Cons of Using VMPI

Pros

- Ability to provide more visibility to issuing banks on customer transaction data

- Prevent visa disputes to a greater degree

- Eliminate retrieval request a.k.a soft chargeback

- Minimize fraud claim chargebacks

- Reduce unknown transaction claims

Cons

- Expose your transaction data to issuers

- Time taken to integrate your CRM with a Certified Facilitator like Chargeback Gurus

- Reliability of your CRM (Since VMPI is real-time,, your CRM must have 99.99% reliability)

The Unknowns in VMPI

VMPI was introduced by Visa in Hong Kong and New Zealand in April 2017 and it was found that VMPI reduced chargeback dispute rates by 14%. Visa is planning on introducing VMPI as a pilot program in US. VMPI is not fully utilized by all issuers in the US and we are yet to see if VMPI can eliminate chargebacks beyond 60% when utilized by all issuers.

As stated before, issuing banks will have more visibility of card holder purchase information, other than just the transaction data. But Visa has not mandated the use of the VMPI program to the issuing banks.

The success of this program purely depends on the usability of the VMPI engine by the issuing banks.

VMPI results have been very welcoming for all CNP merchants. VMPI eliminates the need to issue refunds when a query is raised by the issuer, unlike prevention alerts program which require the merchant to issue a refund to proactively prevent a dispute.

VMPI is less expensive than Prevention Alerts service and we highly recommend merchants to utilize both VMPI and Prevention Alerts services to maximize their prevention. Combining VMPI, Prevention Alerts along with Chargeback Representment, helps merchants prevent what they can and fight what they couldn't prevent. All these three services are proven to minimize chargeback revenue loss and maximize revenue recovery.

Who is VMPI for?

VMPI must be used by any merchant processing credit cards on a card-not-present (CNP) environment. VMPI can certainly be beneficial for these types of merchants:

- Travel

- Entertainment

- Health & Beauty

- Adult

- Digital Goods

- Digital Services

- Any merchant facing a chargeback rate over 0.75%

How Do Merchants Sign Up for VMPI?

Signing up and enrolling for VMPI can be a 5-step process. The steps include:

-

Merchant must complete the Visa Questionnaire Form which must include merchant’s business name, address and merchant identification number (Merchant ID)

-

Merchant must provide CAID (Cardholder Acceptance Identification Number) issued by Visa. This ID can be obtained from your payment processor

-

Merchant must provide acquirer’s BIN (Bank Identification Number). This BIN can be obtained from your payment processor as well

-

VMPI facilitator will connect Merchant's CRM to the VMPI engine after the merchant is approved by Visa

-

A test will be performed by Visa to check the connectivity and data transfer before the merchant account goes live

Merchants can sign up for VMPI directly with Visa or enroll with an Authorized VMPI Facilitator.

Conclusion

If you would like more information on VMPI and the recent Visa Claims Resolution (VCR) policy updates, download the 7-Part Definitive Guide to Visa's New Dispute Process.

FAQ

How do you when a chargeback as a merchant?

How many chargebacks are too many

Is it better to refund a customer or dispute a chargeback?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com.