FAQ: Ethoca Chargeback Alerts

Table of Contents

- The Problem of Chargebacks

- What Are Ethoca Alerts?

- What Is Ethoca?

- What Are the Benefits of Ethoca Alerts?

- Is Ethoca the Only Company That Provides Chargeback Alerts?

- Why Let a Chargeback Management Company Handle Alerts For You?

- How Long Does it Take to Set Up Chargeback Alerts?

- Prevention Rates for Chargeback Alerts

- Are Chargeback Alerts the Best Way to Prevent Chargebacks?

Merchants should always be looking for ways to reduce the number of chargebacks they get. Whether they're legitimate or not, excessive chargebacks can get a merchant cut off by their bank or payment processor. Even simple disputes that a merchant could easily resolve directly with the customer, if given the opportunity, can turn into chargebacks that have a lasting negative effect on a business.

Ethoca alerts work to reduce chargebacks by intercepting cardholder disputes at their point of origin with the issuing bank, sending a chargeback prevention alert to the merchant, and giving them a chance to resolve the dispute before it moves on to the chargeback stage.

The Problem of Chargebacks

If the ratio exceeds a certain threshold and stays there, the merchant may be added to a program like the Visa Acquirer Monitoring Program (VAMP). The merchant will then be charged additional fees for each chargeback they receive.

Their acquiring bank may also take various actions, such as imposing a higher reserve requirement or even terminating the merchant account altogether.

Merchants whose accounts are closed due to a high chargeback ratio may be unable to open a new merchant account with a different bank, leaving them with expensive, high-risk payment processing companies as their only option.

Unfortunately for merchants, "friendly fraud" chargebacks are becoming more common, as customers initiate chargebacks with their banks for the sake of convenience rather than attempting to resolve their issue with the merchant directly first. These customers may not realize it, but these chargebacks can have serious consequences for merchants who lack any type of chargeback protection. That's where Ethoca alerts come in.

What Are Ethoca Alerts?

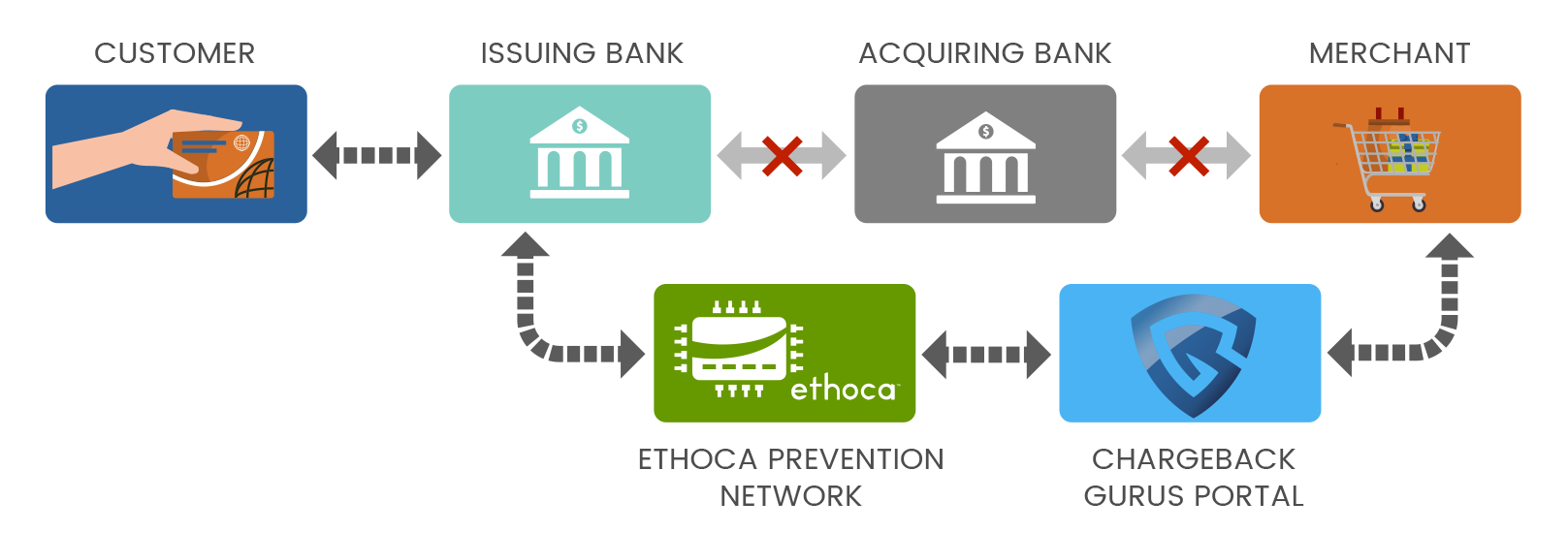

Consider a chargeback as it happens. The cardholder approaches their bank claiming that a charge on their account is fraudulent. The bank investigates, and if they find sufficient cause, they will initiate a chargeback and reverse the transaction.

Banks that are part of a chargeback alert network like Ethoca will notify the alert provider before taking that final step.

The alert provider then notifies the merchant. The merchant can then stop fulfillment of the order if it hasn't already been completed and issue a refund to the cardholder, negating the need for a chargeback.

For merchants, a refund is almost always preferable to a chargeback. Refunds don't come with chargeback fees or threaten your merchant account. However, if the merchant has evidence that the cardholder's dispute is illegitimate, they can still choose not to issue a refund and instead fight the chargeback through representment.

What Is Ethoca?

Ethoca's network allows them to bring cardholder problems to merchants' attention quickly, sending chargeback prevention alerts that essentially hit the "pause" button on the chargeback process, giving merchants the chance to resolve issues without involving the acquiring bank.

What Are the Benefits of Ethoca Alerts?

By issuing a refund directly in response to an alert, the merchant's chargeback ratio remains unchanged, at least most of the time. If the dispute was raised as a fraud claim and the issuing bank chooses to file a TC40 report, that can still count against a merchant's VAMP ratio. However, by preventing a dispute from being added to the count, the VAMP ratio will still be lower than it would be without alerts.

This is the key benefit of chargeback prevention alerts. Although each alert comes with a fee that may offset the benefit of avoiding chargeback fees, an excessive chargeback ratio can have much greater consequences for merchants.

If a merchant exceeds the chargeback ratio or VAMP ratio that the card network has established for three consecutive months, they may be enrolled in a monitoring program, resulting in fees that may significantly outweigh the cost of chargeback alerts.

Additionally, merchants can still recover revenue lost to chargebacks even when enrolled in alerts. If a merchant gets an alert for a dispute that they want to fight, they can decline to issue a refund, and the dispute will proceed as a chargeback.

Is Ethoca the Only Company That Provides Chargeback Alerts?

The other major company that provides prevention alerts is Verifi, which is owned by Visa. Both companies maintain agreements with large networks of issuing banks around the world.

There is considerable overlap between the two networks, but there are differences. While both companies have global networks, Ethoca has stronger coverage among Canadian, European, and Asian banks, while Verifi's network is more robust within the United States. Neither company's network is limited to the card brand that owns it. Some banks that issue Visa cards will be on Ethoca's network and vice versa.

Both companies charge a fee any time an alert is sent out, and they both require merchants to take action on an alert within a short time of receiving it. Verifi CDRN gives merchants 72 hours to initiate a credit. Ethoca instructs merchants to respond within 24 hours to optimize the chance of preventing a chargeback.

If an alert isn't handled quickly enough, it goes through the full chargeback process, and the merchant is still required to pay the alert fee.

Signing up for both Ethoca and Verifi gives merchants the broadest possible range of bank coverage, but because of the overlap between networks, merchants will get some duplicate alerts.

Whether to sign up with both companies or just one depends on where your customers are located and how important preventing chargebacks is for your business.

Why Let a Chargeback Management Company Handle Alerts For You?

In addition to signing up with Ethoca or Verifi directly, merchants also have the option of obtaining these services through a third-party provider such as Chargeback Gurus, which can integrate these alerts into a single platform alongside the other services it provides.

Here are a few reasons merchants might want to consider this option:

- Working with a chargeback management company that is an authorized reseller of Verifi and Ethoca prevention alert programs means that you can get coverage from both services through a single provider.

- When you hire a chargeback management company, you can have a dedicated team that responds to chargeback prevention alerts within the required time frame. That way you never have to worry about failing to respond in time and having to pay for both the alert and the chargeback.

- Some chargeback management companies provide an intuitive dashboard where you can manage the alerts from different networks in one portal rather than logging in to multiple systems to track your prevention alerts.

- A chargeback management company may even offer a 100% chargeback prevention guarantee when a prevention alert is handled. This means if an alert, after issuing a refund, still turns into a chargeback, the management company will refund 100% of your alert fee.

- A chargeback management company may be able to offer the same rates that are charged by the alert networks themselves, providing these additional benefits at no additional cost.

How Long Does it Take to Set Up Chargeback Alerts?

- New merchants: 45 – 60 days

- Existing merchants setting up alerts: 20 – 30 days

- Existing merchants switching alert providers: No delay

To enroll in the prevention alert network, the merchant must provide:

- Merchant/Business name

- Official registered address for the business

- Merchant account descriptor (customer credit card statement name)

- Merchant account number (the ID provided by your payment processor)

- Access to merchant’s sales system (to issue refunds and resolve alerts)

Prevention Rates for Chargeback Alerts

There are a number of factors that can influence how many chargebacks will be intercepted by prevention alerts. For example, merchants with more customers in the US will have better coverage, since a higher percentage of issuing banks in the US are enrolled in alert networks.

Prevention will also vary based on the type of product or service associated with the transaction. Here are some benchmarks based on Chargeback Gurus data:

| Product Category | Percent of Chargebacks Prevented with Ethoca Alerts |

| Physical Goods | 32% |

| Digital Goods | 64% |

| Digital Service | 53% |

| Subscriptions | 61% |

Are Chargeback Alerts the Best Way to Prevent Chargebacks?

By addressing the real causes of chargebacks, merchants will save money in the long run. Here are a few basic steps that can help reduce the occurrence of chargebacks:

- Offer realistic expectations for your products and services.

- Provide customers with terms of service and refund terms before purchases are made.

- Make it easy for customers to get in touch with customer service and to cancel their orders or subscriptions.

- Use a billing descriptor that customers will recognize.

Of course, the best prevention strategy will involve analyzing your company's chargeback data to identify specific causes and trends. With that insight, merchants can make targeted changes to policies, processes, fraud controls, and customer communications while reserving alerts for the disputes that cannot be prevented earlier in the transaction lifecycle.

Used together, data-driven prevention and timely alert responses can give merchants greater control over chargeback ratios while supporting a more sustainable approach to chargeback management.