FAQ: Verifi CDRN Chargeback Alerts

Table of Contents

- What is a chargeback alert?

- What are the consequences of chargebacks?

- What are Verifi CDRN alerts?

- What are the benefits of Verifi chargeback alerts?

- Is Verifi the only company that provides these notifications?

- Why let a chargeback management company handle alerts for you?

- How long does it take to set up chargeback alerts?

- What percentage of chargebacks can CDRN alerts prevent?

- What do I need to get started with a prevention alert network?

- Are alerts the only way to prevent chargebacks?

- How much do chargeback alerts cost?

Looking for ways to reduce chargebacks? You should be! Too many chargeback requests can cost a merchant access to credit card payment processing services, even if the chargebacks don't turn out to be legitimate. This can be especially frustrating when a chargeback is initiated for a transaction that the merchant would have been willing to refund if the customer had asked them first.

One way to reduce the number of chargebacks you receive is through the chargeback prevention alerts available from companies like Verifi. These companies establish large networks of banks that will notify them of cardholder disputes, allowing them to provide merchants with alerts that can enable them to circumvent the chargeback process and issue refunds without getting the banks involved.

What is a chargeback alert?

For example, consider a situation where a customer is dissatisfied with their purchase and is struggling to get in contact with the merchant due to a mismatch in availability or method of communication. Unable to get their needs met, the cardholder goes to their bank to get the charge reversed, claiming either merchant error or some other problem.

If the customer's bank is part of an alert network, they will send a notification through the network before proceeding with a chargeback. If the merchant is signed up for chargeback alerts through the same network, they'll receive an alert. At that point, the merchant can either contact the cardholder to try to resolve the problem or simply issue a refund immediately, notifying the bank they have done so.

If the customer's bank is part of an alert network, they will send a notification through the network before proceeding with a chargeback. If the merchant is signed up for chargeback alerts through the same network, they'll receive an alert. At that point, the merchant can either contact the cardholder to try to resolve the problem or simply issue a refund immediately, notifying the bank they have done so.

What are the consequences of chargebacks?

Merchant whose chargeback ratio exceeds certain thresholds can be enrolled in corrective programs like the Visa Dispute Monitoring Program (VDMP). Those categorized as high-risk and those who stay above those thresholds for four months can start being charged additional fees for every chargeback as well as a large monthly fee that increases the longer a merchant stays in the program.

If the problem continues for too long, the merchant's acquiring bank may terminate their merchant account and add them to the MATCH list, an industry-wide blacklist used by banks and payment processors.

Most banks and processors aren't interested in doing business with merchants on the list, considering them too high-risk. The few that will often specialize in dealing with high-risk merchants, charging much higher fees and placing additional restrictions on merchant accounts.

Different types of businesses may have different chargeback thresholds before they're considered too risky — a small brick-and-mortar store may have more leeway than a high-volume online retailer, for example.

If a merchant starts to look like a high risk, some acquiring banks may even start putting restrictions on their monthly processing volume, hold funds in reserve to guard against chargeback losses, or even terminate accounts before the threshold for excessive chargebacks is reached.

It's becoming more common these days for customers to initiate chargebacks with their banks before they've even tried reaching out to the merchant to resolve their issue. These customers might not have malicious intentions, but this "friendly fraud" can still have dire consequences for merchants who don't have any kind of chargeback protection.

What are Verifi CDRN alerts?

Based in Los Angeles and founded in 2005, Verifi is a company that provides payment protection and management services for eCommerce companies.

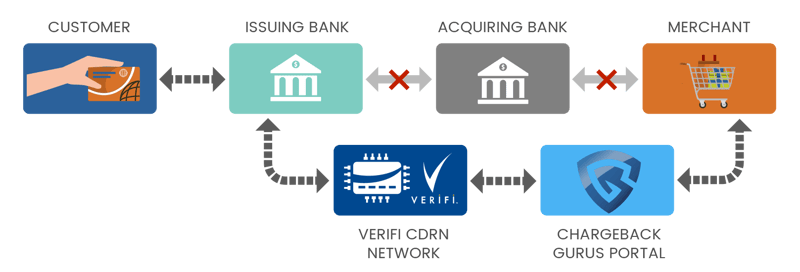

Their CDRN receives immediate notifications from issuing banks about cardholder issues, which allows them to alert merchants, giving merchants the chance to resolve these issues before they become chargebacks (as seen below).

These CDRN notifications effectively freeze the chargeback process for 72 hours and give the merchant the first opportunity to deal with the customer's problem. The merchant can choose to give the customer a refund and resolve the issue or do nothing and allow it to proceed as a chargeback, which they can then dispute if they believe it to be illegitimate or fraudulent.

What are the benefits of Verifi chargeback alerts?

Verifi charges users a fee for every alert they receive from the CDRN, regardless of how they choose to handle the issue. However, these fees are well worth it for merchants who are in danger of having their accounts terminated and ending up on a blacklist.

Is Verifi the only company that provides these notifications?

Another company that offers chargeback prevention alerts is Ethoca, which is based in Canada. Both Verifi and Ethoca work with a large network of issuing banks to identify cardholder disputes in real time, and while there is significant overlap between the two networks, they are not identical. Verifi currently has better coverage in the United States and is working to expand their network, while Ethoca covers more banks from Canada, Europe, and Asia.

Both companies charge a fee whenever an alert is issued. If an alert isn't dealt with on time, it proceeds as a chargeback, but the merchant is still obligated to pay the fee.

Signing up with both Verifi and Ethoca gives merchants the widest range of coverage for chargeback prevention alerts, but because most of the largest issuing banks are included in both networks, merchants who sign up with both might receive duplicate alerts and have to pay twice the fees.

Why let a chargeback management company handle alerts for you?

Working with a chargeback management company that's an authorized reseller of Verifi and Ethoca prevention alert programs means that you have the coverage of both Verifi and Ethoca, and one unified system to manage your alerts effectively.

When you hire a chargeback management company, you have a dedicated team that responds to chargeback prevention alerts within the required time frame. This way you never have to worry about failing to respond in time. When a merchant signs up for alerts directly with the networks, the burden of resolving the alerts promptly falls on the merchant.

Some chargeback management companies provide an intuitive dashboard where merchants can manage the alerts from different networks in one portal rather than logging in to multiple systems to view prevention alerts.

A chargeback management company may even offer a 100% chargeback prevention guarantee when a prevention alert is handled. This means if you issue a refund and the alert still turns into a chargeback, the management company will refund your alert fee.

A chargeback management company may even offer a 100% chargeback prevention guarantee when a prevention alert is handled. This means if you issue a refund and the alert still turns into a chargeback, the management company will refund your alert fee.

Lastly, a chargeback management company may charge the same fee that is charged by the alerts networks, providing all these additional benefits for the same alert cost.

How long does it take to set up chargeback alerts?

- New merchants who haven't processed any transactions yet: 15 – 30 days

- Existing merchants who are signing up for alerts for the first time: 7 – 10 days

- Existing merchants who are switching alert providers: 1 day

What percentage of chargebacks can CDRN alerts prevent?

The number of chargebacks that can be halted by the prevention alert networks depends on several factors, including:

- Transaction count (Coverage increases as the number of transactions goes up)

- Location of customer bank (Customer base within the U.S. has better coverage than overseas)

- Years in operation (businesses that are more established generally have better coverage than newer merchants)

Based on our internal data analysis, here are the percentages of chargebacks that each alert network can be expected to prevent:

|

Service/Product |

Verifi |

Ethoca |

|

Physical Goods |

21% |

17% |

|

Digital Goods |

41% |

30% |

|

Digital Service |

17% |

33% |

|

Subscription Industry |

19% |

14% |

What do I need to get started with a prevention alert network?

To have your merchant accounts successfully enrolled in the prevention alert network, you must provide:

- Business/merchant name

- Registered address of the business

- Merchant descriptor (name as seen on customer credit card statements)

- Merchant account number (ID provided by your payment processor)

- Access to your sales system (for refunds and alert resolution)

Are alerts the only way to prevent chargebacks?

Using chargeback alerts can be costly. Here is an example of the kind of costs a merchant could see when refunding a potential chargeback through an alert network:

|

Transaction Amount |

$100.00 |

|

Cost of Goods |

$25.00 |

|

Fulfillment Costs |

$8.00 |

|

Marketing Cost |

$25.00 |

|

Processing Fee |

$3.50 |

|

Operations Fee |

$10.00 |

|

Prevention Alert Fee |

$40.00 |

|

Total Cost |

$211.50 (Over 2x the cost of the Transaction Amount) |

If you’re aiming to prevent chargebacks, here are five steps you can follow to reduce them organically over the long term:

- Set realistic expectations for your products and services.

- Ensure you have stellar customer service practices in place by providing quick responses to all phone calls and emails.

- Provide both terms of service and refund terms to customers before transactions.

- Make it simple for customers to reach customer service, or to cancel their order or subscription.

- Address any internal issues that trigger chargebacks.

If you're not sure whether or not chargeback alerts are the right solution for you, you can consult with a chargeback management company. These experts can provide expert advice, support, and customized tools to help you prevent and fight chargebacks in whatever way will work best for your business.

FAQ

How much do chargeback alerts cost?

Thanks for following the Chargeback Gurus blog. Feel free to submit topic suggestions, questions or requests for advice to: win@chargebackgurus.com