The Complete Guide to the Chargeback Process

Key Takeaways:

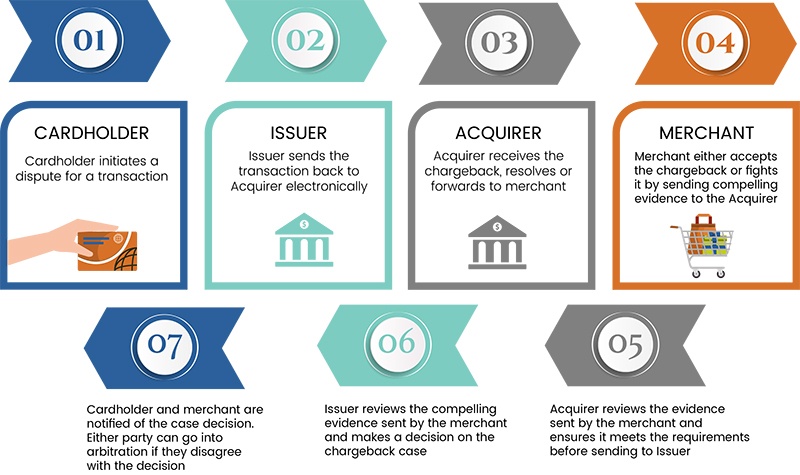

Chargeback Process: A chargeback begins when a cardholder or issuer disputes a transaction. The issuer, card network, acquirer, and merchant may all participate as the case moves through notification, acceptance or representment, issuer review, and possible escalation.

Merchants Must Respond: After receiving a chargeback, the merchant must either accept liability or submit representment by the applicable deadline. Failing to respond generally closes the opportunity to contest the dispute and may result in an additional fee.

Evidence Drives Representment: Merchants fighting a chargeback should submit a rebuttal letter and compelling evidence that addresses the reason code. Relevant records may include authorization data, transaction timestamps, delivery verification, customer history, communications, and signed receipts.

Winning Has Limits: A successful representment may return the transaction amount, but the original chargeback fee may remain and the dispute may still affect the merchant’s chargeback ratio. Prevention therefore remains important even when recovery performance is strong.

Prevent Recurring Disputes: Clear billing descriptors, transparent policies, responsive customer service, accurate fulfillment, prompt refunds, fraud controls, and chargeback analysis can address root causes before they produce additional disputes.

The chargeback process is similar across most credit card networks and issuing banks, with specific differences for each bank or network. A chargeback works its way from the issuing bank through the card network and to the merchant's acquiring bank. The merchant can decide to dispute the chargeback or accept it.

A chargeback may begin simply enough when a cardholder contacts their bank to dispute a charge, but the merchant can fight the chargeback, banks can challenge each other’s decisions, the card networks can get dragged in to adjudicate—things can get messy. What do merchants need to know about navigating the chargeback process?

- Who Are the Participants in the Chargeback Process?

- What Is the Chargeback Process?

- How Can Merchants Fight Chargebacks?

- What Happens When You Accept a Chargeback?

- What Are the Best Ways to Prevent Chargebacks?

- Solving the Chargeback Puzzle

A chargeback isn’t just a single event. It’s a process, one that can be lengthy and convoluted for all parties involved. For merchants, chargebacks are especially troublesome, because the lion’s share of the liability for chargebacks falls on them.

It doesn’t help that the chargeback process is largely defined by regulations that were written out long before the age of e-commerce, and that each card network creates its own rules based on their interpretation of those regulations.

Understanding how the chargeback process works isn’t just for personal edification. Knowing the ins and outs of the process can help you avoid costly mistakes, fight fraudulent chargebacks more effectively, and get a better ROI on the time and labor you spend on dealing with disputes.

Here’s what you need to know about the chargeback process.

Who Are the Participants in the Chargeback Process?

- The cardholder/ customer

These may be the same individual, but not always. The cardholder is the actual owner of the payment card used to make the purchase under dispute. The customer is the individual who placed the transaction.

In a typical transaction, or in a friendly fraud chargeback, the cardholder and the customer are the same person. In a true fraud scenario, the customer who made a transaction with a stolen card is not the same person as the cardholder who disputes it later. - The merchant

The merchant is the individual or company who sold a product or service to the customer. When the chargeback is filed, the merchant must decide whether to accept it or dispute it. - The issuing bank (Issuer)

A bank or other financial institution that issues a branded payment card to the cardholder. Examples: Bank of America, Wells Fargo, Capital One. - The acquiring bank (Acquirer)

The merchant’s bank, which holds their merchant account and enables them to accept credit card payments. - The credit card network

The association that owns the credit card brand used in the transaction. In the United States, the four major credit card networks are Visa, Mastercard, American Express, and Discover. These networks set the terms for credit card transactions, which are followed by the issuing banks.

Other companies that service merchant accounts, such as payment processors and payment gateways, may also become involved in the chargeback process.

What Is the Chargeback Process?

When a chargeback is accepted, the cardholder keeps the returned funds and the case is closed. If the merchant chooses to fight back with representment, the issuing bank will review any evidence that the merchant sends along and decide whether or not to reverse the chargeback. If the issuer upholds the chargeback, the case can be appealed to the card network.

Merchants must be aware of the responses required of them and the deadlines for those responses, which will differ from network to network, and can be complicated further by factors such as chargeback alert or deflection services. However, a basic chargeback process can easily be outlined. Just be aware that some chargebacks will deviate from this formula:

- The cardholder comes to believe that a transaction made to their account is invalid and they should not have to pay it. They contact their issuing bank to dispute the transaction.

- The issuing bank listens to the cardholder’s claim and determines whether it constitutes a valid reason to grant a chargeback. If the claim is invalid, the dispute will go no further and no chargeback will occur.

Most banks, however, extend the benefit of the doubt to their customers and will allow the chargeback in most cases, so long as the customer's reason for the dispute falls under one of the approved categories. The issuing bank gives the cardholder a provisional credit equal to the disputed transaction amount. - The bank then notifies the merchant's acquirer. Once the acquiring bank is notified, they will debit the merchant’s account and charge them any applicable chargeback fees.

The acquiring bank will notify the merchant about the chargeback. This can be some time out from the initial dispute, and is usually the first the merchant hears about it. - The merchant must then decide whether to accept or fight the chargeback. If the merchant chooses to fight the chargeback, they must submit a rebuttal letter and supporting evidence to prove that the dispute is invalid.

- The acquirer will pass along the merchant's submitted dispute package to the issuer.

- The issuing bank will evaluate this evidence and decide whether to reverse or uphold the chargeback.

- If the bank decides against the merchant, the merchant can appeal through arbitration, at which point the card network steps in to decide the case. The losing party in arbitration will be charged hundreds of dollars in fees.

Merchants should also note that if they fail to either fight or accept a chargeback by the deadline, they may be charged an additional non-response fee on top of the regular chargeback fee. Thus, every chargeback requires a response of some sort, even if the merchant doesn't want to fight it.

How Can Merchants Fight Chargebacks?

A represented charge will only be accepted by the issuing bank if the merchant includes compelling evidence that refutes the cardholder’s dispute claims. The right evidence will depend entirely on the substance of the claims, but for typical chargebacks relevant evidence may include:

- Transaction data including a date and timestamp

- AVS, CVV, and delivery verification

- The cardholder’s transaction history

- Communications between the merchant and the cardholder

- Signed delivery receipts

- Other pertinent data or documentation related to the transaction being disputed

The merchant’s evidence will be passed along from the acquirer to the network to the issuer, who will review it and make a decision. If the issuer finds the merchant’s evidence valid and compelling, they will reverse the chargeback by taking away the cardholder’s provisional credit.

The acquirer will then return the merchant’s funds to their account. However, the chargeback fee will not be refunded, and the chargeback will still count toward the merchant's chargeback ratio. That's why prevention is always the best cure for chargebacks.

If the issuer does not believe that the merchant’s evidence disproves the cardholder’s claim, the chargeback will stand. While merchants can appeal the case by requesting arbitration from the card network, it isn’t usually a good idea to do so. The card network will often evaluate the evidence similarly to the issuer, and when a case goes to arbitration, the losing party will have to pay hundreds of dollars in fees.

What Happens When You Accept a Chargeback?

If the merchant fails to submit a response by the deadline, the merchant will accept the chargeback by default.

Merchants may decide to accept chargebacks for several reasons. Sometimes the chargeback is based on true fraud or some other valid and inarguable reason, and there is no point in trying to fight it. If the chargeback is the result of merchant error, for example, then by the time the chargeback has been initiated it's already too late to go back and fix the problem. If the cardholder's claims are true, the merchant won't be able to disprove them.

Many merchants, however, accept chargebacks because they’re too busy to deal with them, or they’ve become convinced that chargebacks are just an unavoidable cost of doing business.

In truth, few merchants can actually afford to passively absorb chargebacks and ignore their underlying causes. In many cases, they don’t even realize how much damage chargebacks are doing to their business until it’s too late.

With fees and overhead added, chargebacks can cost more than double the original transaction, making them a tremendous drain on a merchant’s revenue.

Once you factor in fees, marketing, and lost overhead, the total cost of a chargeback can be as much as 250% of the disputed purchase amount. Additionally, the chargeback will count against a merchant's chargeback ratio regardless of whether they win or lose.

Fighting chargebacks—especially fraudulent ones—helps merchants recover revenue, discourage repeat offenders, and preserve their reputation with issuing banks, making them less likely to reflexively side against them in future disputes.

The best way to stop chargebacks from taking away your revenue is to prevent them from happening in the first place.

What Are the Best Ways to Prevent Chargebacks?

As the saying goes, an ounce of prevention is worth a pound of cure, and that's especially true of chargebacks. Not only do chargebacks cost businesses time and money, they also increase a merchant's chargeback ratio, win or lose. If that ration gets to high, merchants can face higher fees and even account termination and blacklisting if the problem goes on too long.

Fortunately, banks don't want to deal with chargebacks either, and they do make some small efforts to encourage cardholders to address any problems by contacting the merchant.

Even Capital One, a major issuing bank, has a chargeback guide for cardholders that emphasizes working with merchants to resolve problems before requesting a chargeback.

What does this mean for merchants?

Practice honesty and transparency with your customers. If they have a complaint about their purchase, your service, or a transaction, make sure that you respond promptly to their concerns and stay in touch until you can work out an acceptable solution. Keep them informed about the refund process if they are going to be receiving one, and make sure that customer service makes it easy for them to resolve problems with you.

Also, take advantage of the fraud prevention tools available to you. Don't wait for fraud to reach a crisis point. Fraud prevention tools can help automate responses to red flags in the purchase process, blocking fraud attempts before they can be completed. By preventing true fraud, you can avoid future chargebacks.

Understanding Pre-Arbitration and Second Chargebacks

While many merchants are familiar with the initial representment stage, fewer fully understand what happens when a dispute escalates into pre-arbitration or a second chargeback.

Pre-arbitration occurs when the issuing bank, after reviewing the merchant’s representment evidence, decides to re-open the case because the cardholder has provided additional information or new claims. This step can catch merchants off guard because it reintroduces a dispute they believed was already resolved.

If the merchant disagrees with the pre-arbitration decision, they can take the case to arbitration, where the card network makes a final ruling. Arbitration comes with significant fees, so merchants often weigh the transaction value against the potential cost of losing before proceeding.

The merchant should carefully review the updated information submitted by the issuer. Going to arbitration with the same documents from the first representment round is rarely enough—new evidence or additional context may be needed to address the cardholder’s revised claims.

For example, if the dispute reason code changes from “merchandise not received” to “merchandise not as described,” the merchant might need to include a product description that proves the item was described accurately.

In cases where the reason for the claim hasn't changed, the merchant may not have any additional relevant evidence to submit. In these cases, it's often best to accept the pre-arbitration decision to avoid incurring further fees. However, if the chargeback is of a particularly high value and the merchant feels the issuer disregarded strong evidence, it may still be worth pursuing arbitration.

Solving the Chargeback Puzzle

The chargeback process can be a long and winding road indeed, and the best way to deal with chargebacks is to avoid them in the first place.

Aside from the constant threat of lost revenue, chargebacks can endanger merchants by putting their merchant accounts at risk. If you carry an excessive chargeback rate for too long, you might not be able to find any reputable payment processors willing to work with you.

Brick-and-mortar merchants can avoid many chargebacks simply by using payment terminals with EMV chip readers. For e-commerce merchants, prevention can be more of a challenge, but standardizing the procedures and protocols for credit card payments can be an important first step in avoiding authorization and fraud chargebacks. Anti-fraud software tools can be a big help too.

To protect themselves, merchants must always be vigilant about reviewing their operations, policies, and even their marketing materials for potential chargeback vulnerabilities. Investing in the services of chargeback management specialists can assure merchants of greater success in these tricky endeavors.