Chargebacks 101: A Merchant’s Guide

Originally created to protect consumers from fraud, credit card chargebacks now pose a challenge for merchants, who often face losses and operational difficulties when disputes arise. In this article, we’ll give you the facts about chargebacks and cover strategies that merchants can use to manage and reduce their occurrence.

What Is a Chargeback?

A chargeback is a reversal of a card transaction, typically initiated by the cardholder through their issuing bank. The system was designed as a consumer protection mechanism, ensuring that cardholders could address issues such as fraud or billing errors.

For merchants, however, chargebacks introduce substantial costs, as they lead to a loss of revenue and incur additional fees.

Chargebacks are a common occurrence across many industries, and recent years have shown a steady increase in these cases as more transactions take place online. Merchants need to understand how chargebacks work to better respond to disputes and reduce their impact on business.

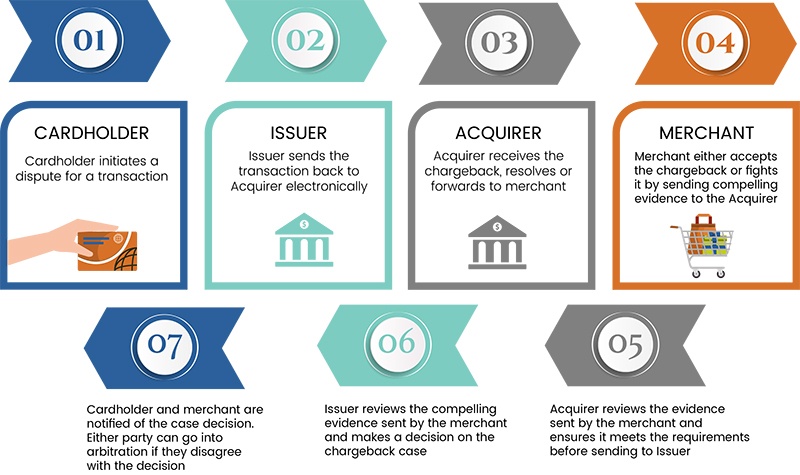

The Chargeback Process

The chargeback process begins with the cardholder disputing a charge by contacting their issuing bank. The bank reviews the cardholder’s claim to determine if it appears valid and, if so, provides a provisional credit to the cardholder and debits the appropriate funds from the merchant’s account.

The merchant has the option to accept the chargeback or contest it through a process known as representment. During representment, the merchant submits evidence to prove the transaction was valid. The issuing bank then reviews the evidence and decides whether to uphold or reverse the chargeback.

Some chargebacks go beyond representment and enter pre-arbitration if one of the parties presents new evidence or challenges the representment outcome. If pre-arbitration does not resolve the dispute, the case may escalate to arbitration, where the card network makes a final decision. Arbitration can be costly, with fees often in the hundreds of dollars, so merchants usually aim to avoid this step unless they have strong evidence in their favor.

Types of Chargebacks

There are three primary types of chargebacks, each requiring different approaches from merchants.

True Fraud Chargebacks

These occur when a cardholder’s payment information is used without their consent, typically due to identity theft or stolen card details. True fraud chargebacks are challenging for merchants to dispute successfully because they generally involve unauthorized transactions. Instead, merchants can focus on preventing these by using fraud detection tools.

Friendly Fraud Chargebacks

In cases of friendly fraud, the customer disputes a legitimate transaction, often claiming it was unauthorized or fraudulent. While friendly fraud can sometimes result from genuine confusion, it is also used by customers attempting to avoid payment for products or services.

Representment is often an effective method for contesting these chargebacks, as merchants can submit transaction records, delivery confirmation, and other evidence to prove the purchase was legitimate.

Merchant Error Chargebacks

These chargebacks stem from mistakes made by the merchant, such as sending the wrong item, failing to deliver an order, or overcharging. Merchant error chargebacks are preventable with improved quality control and clear communication with customers.

Estimated occurrence of chargeback types

Chargeback Fees and Financial Impact

The cost of a chargeback extends well beyond the lost sale. Each one incurs a chargeback fee which can range from $5 to $100 per dispute depending on the merchant’s perceived risk and ability to negotiate lower fees. The merchant also faces indirect costs, including the time spent gathering documentation, lost inventory, and marketing expenses associated with acquiring that customer.

The true cost of a chargeback is often estimated to be 2 to 2.5 times the original transaction amount. For example, a $100 chargeback could lead to losses of up to $250 when accounting for all associated expenses.

Chargeback Ratios

The chargeback ratio is a measure of how often a merchant’s transactions result in chargebacks, typically expressed as a percentage of total transactions monthly. High chargeback ratios can have serious consequences, as card networks often impose limits on the number of allowable chargebacks.

A high chargeback ratio can threaten a business’s cash flow, as acquirers may increase reserve requirements for merchants with excessive chargeback ratios or even terminate accounts entirely in extreme cases.

Chargeback Representment

When a merchant believes a chargeback is unjustified, they have the right to dispute it through the chargeback representment process. During representment, the merchant submits a rebuttal letter and relevant documentation to the issuing bank, explaining why the chargeback is unwarranted.

The representment process begins with gathering all relevant documentation, such as sales receipts, shipping confirmations, and communication records. This evidence is sent to the merchant’s acquiring bank, which then forwards it to the issuing bank for review. If the bank finds the evidence convincing, the chargeback is reversed, and funds are returned to the merchant.

Chargeback Reason Codes

Every dispute comes with a chargeback reason code that categorizes the claim the cardholder made to the bank. Major credit card networks like Visa and Mastercard each have their own sets of reason codes, which help clarify whether the dispute is due to fraud, a processing error, customer dissatisfaction, or another issue.

Understanding these codes is fundamental to managing chargebacks, as they outline the type of evidence the merchant must provide to contest the charge.

A strong chargeback rebuttal letter is concise and well-organized, addressing the specific reason code for the chargeback. Merchants should avoid unnecessary details and instead focus on providing clear, relevant evidence that disproves the customer’s claim.

Chargeback Time Limits

Each credit card network sets chargeback time limits dictating how long merchants have to respond to disputes. These time limits vary based on the network. Missing these deadlines results in an automatic loss of the dispute and can even result in additional fees, highlighting the need for merchants to act promptly.

Maintaining detailed transaction records, including order confirmations and tracking information, is crucial for successful representment. Having a robust documentation system in place allows merchants to respond quickly and thoroughly to disputes.

How to Prevent Chargebacks

Merchants can prevent chargebacks by taking proactive steps to address common chargeback causes.

Fraud Detection Tools

Implementing tools like Address Verification Service (AVS), Card Verification Value (CVV) checks, and 3-D Secure authentication can help verify that the cardholder is the legitimate user. These tools add security layers, deterring fraudsters and reducing the chances of unauthorized transactions.

Customer Service Optimization

Many chargebacks stem from customer dissatisfaction that could have been resolved directly. By offering responsive customer service, merchants can often resolve issues before a customer feels the need to contact their bank.

Providing multiple customer support channels, such as phone, email, and chat, helps customers find assistance quickly, lowering the likelihood of disputes. In addition, offering generous refund policies or making exceptions for repeat customers or those who haven’t requested a refund before can help avoid chargeback fees.

Clear Policies and Billing Descriptors

Chargebacks can result from misunderstandings regarding policies, particularly in regard to refunds and additional fees. Merchants should ensure these policies are communicated clearly to customers. Additionally, merchants should use recognizable billing descriptors to prevent customer confusion over transactions they see in their account statements.

Chargeback Analytics

Regularly analyzing chargeback data allows merchants to identify trends and recurring issues. By analyzing patterns, merchants can pinpoint specific products, locations, or customer service practices that may be contributing to chargebacks. Addressing operational weaknesses such as fulfillment errors or unclear product descriptions can help prevent chargebacks before they happen.

Managing Chargebacks

Effective chargeback management requires a clear approach to dispute management and a focus on long-term prevention strategies. By following consistent procedures and responding to disputes with well-documented evidence, merchants can recover lost revenue from unfounded chargebacks.

Staying informed about changing chargeback rules and industry practices will equip merchants to manage disputes more successfully and reduce future chargeback incidents. A proactive, informed approach to chargeback management can support business growth by minimizing losses and protecting payment channels.